Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 44s

Market Update: This Week's Setup

Over the weekend, geopolitics replaced macroeconomics as the market’s primary catalyst. A major escalation in the Middle East has injected uncertainty across global assets, forcing investors to reassess inflation risks, rate expectations, and the outlook for risk assets. Here's everything you need to know...

Disclaimer: This is not financial or investment advice. You are responsible for any capital-related decisions you make, and only you are accountable for the results.

Executive Summary:

Geopolitical escalation in the Middle East, following the killing of Iran’s Supreme Leader and subsequent retaliation, is now the primary driver of markets, overshadowing upcoming US economic data. The key risk is a prolonged disruption to the Strait of Hormuz, which could push oil prices materially higher, reignite inflation, and reduce the likelihood of near-term rate cuts - creating downside pressure for equities and other risk assets. While Bitcoin has shown relative resilience and short-term metrics have improved, our base case remains a multi-week conflict, elevated oil prices, and further risk-off repricing before a more durable bottom forms.Topics covered:

- This Week's Economic Data.

- Flight to Safety in Markets due to Escalations in the Middle East.

- Bitcoin Holds Up Under Geopolitical Pressure.

- Cryptonary's Take.

This Week's Economic Data

This week's key economic data is Friday's Payrolls and Unemployment Rate. Estimates are for the Unemployment Rate to remain unchanged at 4.3% and for Payrolls to come in positively at 60k jobs added.Should these numbers come in as expected, it would suggest that the labour market is still resilient, and it would likely aid the argument that further interest rate cuts aren't needed imminently. Risk assets wouldn't likely react well to this, despite the labour market being resilient. For risk assets to see a positive reaction, they'd need to see the labour market print be weaker than estimates, but not negative i.e., weak Payroll numbers but not a negative print.

Flight to Safety in Markets due to Escalations in the Middle East

Early Saturday morning, Iran's Supreme Leader Ali Khamenei was killed in Tehran by a joint US-Israeli strike that also killed a number of high ranking IRGC members. This followed a breakdown in negotiations on Friday in Geneva between the US and the Iranians.Since the killing of the Iranian Supreme Leader, Iran has retaliated by firing ballistic missiles and drones at US military assets throughout the region, this includes: Israel, Bahrain, the UAE, Qatar, Saudi Arabia, Jordan and even Oman who mediated the negotiations last Friday in Geneva. In the last 24 hours, strikes have escalated to hitting cities in Israel, alongside tourist destinations in the UAE, and oil facilities in Saudi Arabia.

Whilst the Iranians have retaliated in a meaningful way, many of their missiles and drones have been intercepted. For instance, the UAE has intercepted 152 out of the 165 Iranian ballistic missiles that were detected, along with 506 of the 541 Iranian drone attacks.

When the US attacks on Iran began in the early hours of Saturday morning, Bitcoin fell from $66k to the low $63ks, but price swiftly bounced, particularly when rumours began circulating that Supreme Leader Ali Khamenei had been killed in those strikes. Since then, Bitcoin has been range-bound between $65k and $68k, which is relatively impressive, as many would have expected a risk-off tone in markets upon an elimination of the Iranian Supreme Leader.

This is likely markets doubting the Iranians’ military capability to really retaliate in a hurtful way. Perhaps the Iranians best weapon is to target ships in the Strait of Hormuz, which we've begun to see. Yesterday, several UK and US owned vessels in the Strait were targeted by Iran. This has resulted in hundreds of vessels anchoring in the Gulf and not moving. Alongside this, Maersk is suspending all its shipments through the Strait, whilst insurance costs for these ships in the Strait have skyrocketed.

Whilst the Iranians can't "close" the Strait, they can make it very dangerous for ships to pass through and essentially halt all traffic passing through.

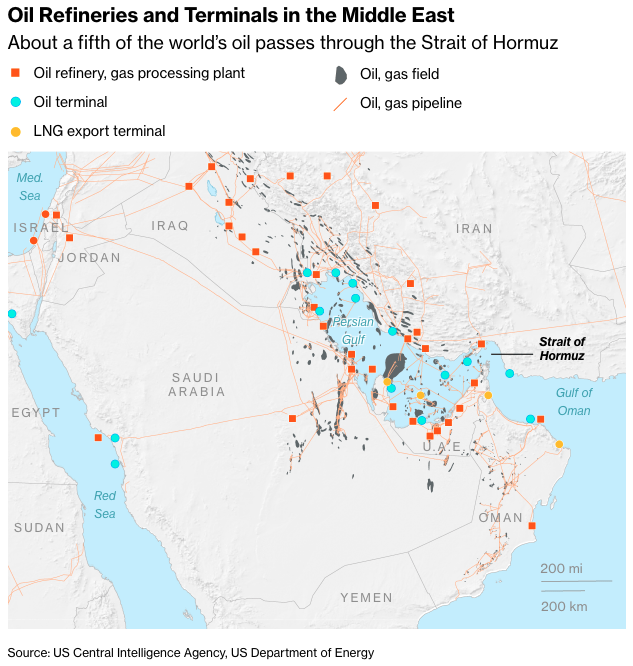

Oil Infrastructure in Middle East:

The above diagram shows the concentration of oil in the region. The world consumes approximately 110 million barrels of oil per day, and approximately 20-25m barrels pass through the Strait. Closing the Strait is arguably the Iranians best weapon.

The immediate impact of closing the Strait is the price of oil rocketing higher. This is hugely inflationary, and is precisely what the Trump administration doesn't want; they're wanting lower inflation so that interest rates can be cut, which in turn stimulates struggling sectors such as housing. This is what markets will likely care about most. Should this be a multi-week, or even multi-month war (whether it results in Iranian regime change or not), elevated oil prices risk de-stabilising US equity markets due to much higher than previously anticipated inflation.

Going into Sunday night’s Futures open, we're seeing a risking off, and a flight to safety in markets.

Oil is up considerably, having touched $82 overnight (up 12% from Friday's close), although price has currently pulled back to $78 (now up 6.8%).

Brent Crude Oil 1D Chart

Meanwhile, the Dollar has been bid, although now pairing back on its gains.

DXY (Dollar Index) 1D Chart

And, Gold is higher, whilst equity indexes such as the Nasdaq are lower, although also recovering slightly in the pre-market trading.

Gold 1D Chart

Nasdaq 1D Chart

Interestingly, Treasuries have been sold (Yields higher), particularly at the front-end. This is likely due to the market anticipating increased issuance (in order to fund a conflict), alongside increased inflationary pressures.

The US2Y Yield is up 0.80%, whilst the US10Y is up 0.48% at the time of writing (Monday's pre-market trading).

US2Y Yield 1D Chart

US10Y Yield 1D Chart

US investors are somewhat programmed to fade geopolitical risk and to 'buy the dip' in risk assets. However, markets are potentially under-pricing the risk currently to a prolonged closing of the Strait of Hormuz. Should the Strait remain closed for a few days, that'll likely stop Brent Crude Oil prices moving beyond the mid-$80s.

However, should the Strait remain closed for several weeks, this'll result in Brent Crude likely moving closer to the $100 mark. Therefore, the Trump administration is likely to put maximum military pressure on Iran this week to alleviate the closing of the Strait, meaning there's unlikely to be off-ramps for the Iranians in the immediate term. The Iranians’ strategy will likely be to keep the Strait closed, putting maximum pressure on the Trump administration to hopefully back down, though this will likely take several weeks.

Either way, we're not expecting an ending to the conflict or de-escalation in the coming days.

In our view, risk assets (Bitcoin and equities) aren't yet pricing in a longer (multi-week) conflict, and are conditioned to 'buy the dip'. Therefore, should we see the Strait of Hormuz remain closed for several weeks, and it might not be until the end of this week that markets realise that's a real possibility, markets would then price in the higher oil prices, the inflationary pressures, and risk assets would re-price lower.

Therefore, we're not in the 'buy the dip' camp.

On the other hand, should we see the conflict resolve in the coming days - and that would likely mean an escalation in terms of military force in the immediate term - and the Strait then reopened again, this would be a signal for risk assets to rally as it would likely mean the end of the conflict and a risk-clearing event.

For now, this isn't our base case.

Our base case is for a multi-week conflict that sees oil prices go higher, inflationary pressures increase, and risk assets to sell-off as a result of this. Though it might take several days/this week for the market to come to this realisation.

Bitcoin Holds Up Under Geopolitical Pressure

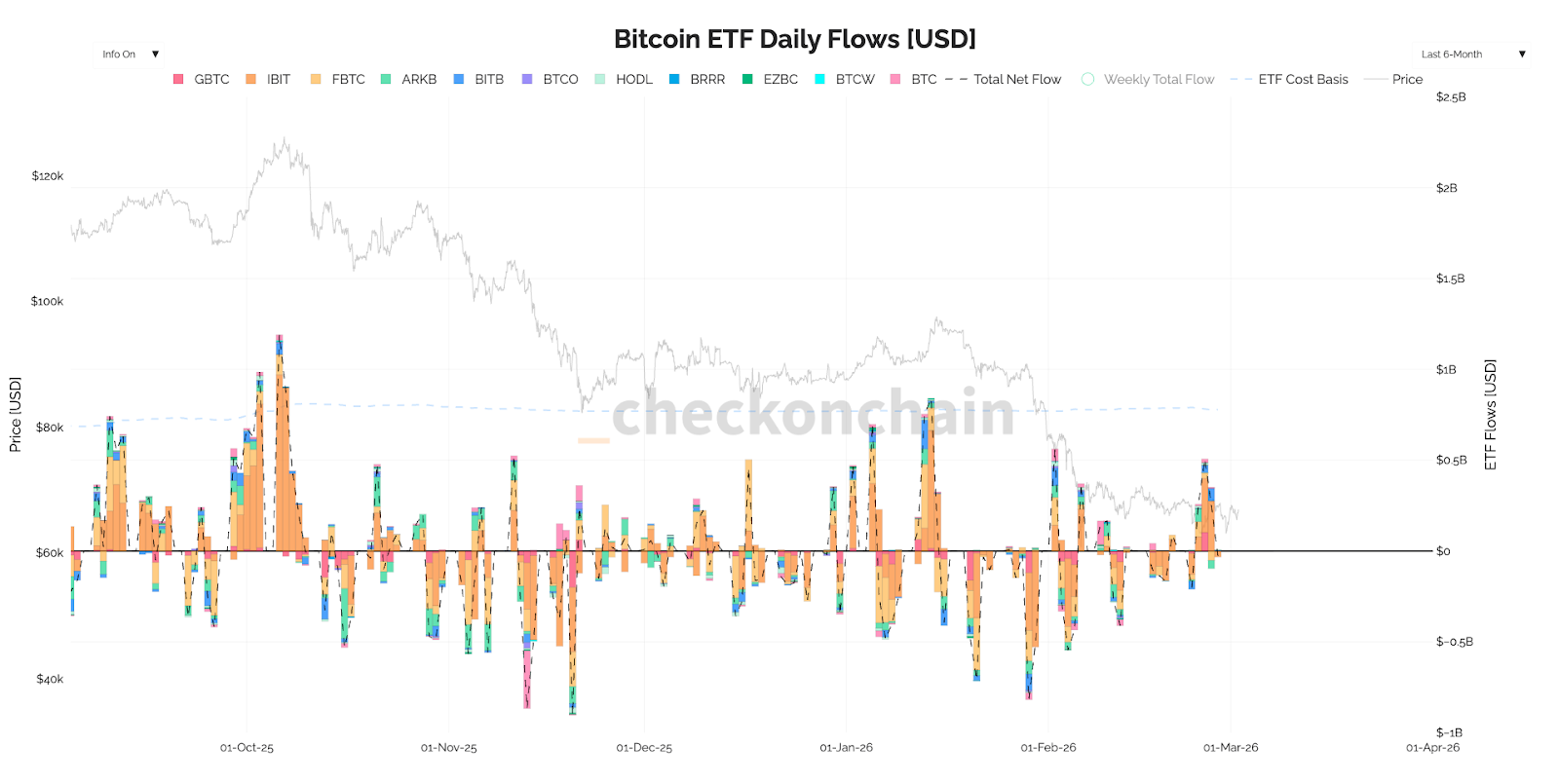

Throughout the weekend, Bitcoin has remained range-bound between $65k-$68k, with a brief move down to the low $63ks on Saturday morning upon the first strikes on Iran.Considering the US and Israel have begun a war with Iran, and taking out their Supreme Leader on the first day of strikes, Bitcoin has held up very well. This also comes off the back of a positive week for the ETFs with inflows at $787.4m over the last week.

Bitcoin ETF Flows

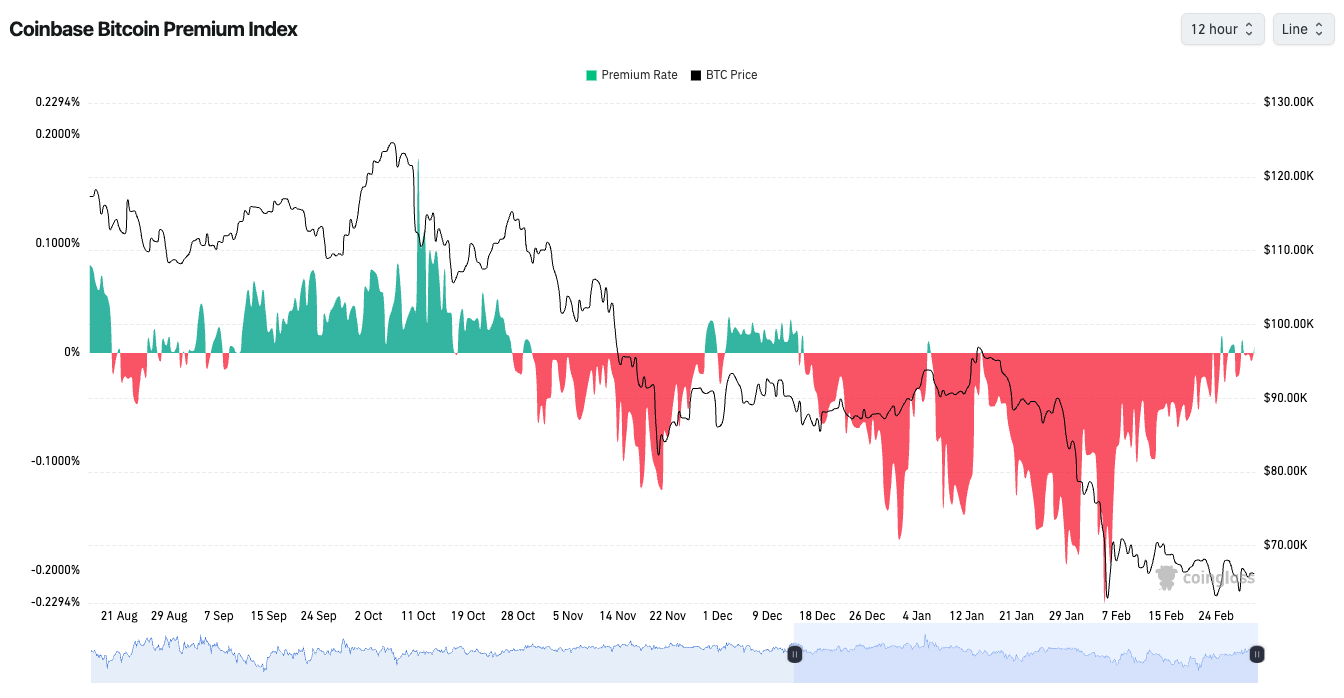

Alongside this, there's a positive Coinbase Premium for the first time in over 40 days.

Bitcoin Coinbase Premium

These are positive developments for Bitcoin and potential price action. When markets don't go up on good news, that should concern participants. When markets stop going lower on bad news, that can be a local bottom for price.

Ultimately, Bitcoin has held the mid-$60ks, despite the extreme geopolitical escalations that we've seen over the last 72 hours. Should the Iranians cave in to the US and Israeli military pressure, and not be able to keep the Strait of Hormuz shut for longer than several days, then risk assets can see some upside, and Bitcoin may see a relief rally.

Unfortunately, we're not sure the conflict in the Middle East will last just several days and we expect it to be multi-week. Should this be the case, risk assets may have room to fall as the market prices in greater inflation via higher oil prices, and in turn, this might bring BTC back into the $60k-$63k zone.

In short: Bitcoin looks better here (in comparison to prior week's), but a move higher is likely dependent on the war in the Middle East being wrapped up in the next few days, rather than it being a more drawn-out conflict.

Cryptonary's Take

Bitcoin has mostly remained range-bound despite huge geopolitical escalations in the Middle East. In the short-term, it's possible that Bitcoin could get a relief rally into the mid-$70ks upon the back of the metrics improving. However, this is likely dependent on the conflict being quickly resolved and the Strait of Hormuz being reopened - not something we see as too likely today.Should Bitcoin retest the $60k-$63k zone due to the conflict, our framework would view that zone as potentially offering asymmetric risk-reward, with the $72k-$75k area as a key resistance zone to monitor should geopolitical pressures abate in the coming weeks.

However, our view remains that Bitcoin could bottom between $50k-$60k in the coming months, as that would align with all prior bear market targets. It just might be the case that we see a rally from $60k-$63k zone into $72k-$75k first off the back of geopolitical pressures abating.

Our proprietary risk framework, combining macro liquidity conditions, on-chain cost basis levels, and derivatives positioning, currently points to a risk-off environment, although a short-term relief rally may be possible.

Key Dates Ahead

- Mar 6: US Nonfarm Payrolls + Unemployment

- Mar 11: CPI

- Mar 17–18: FOMC meeting

This content is for informational and educational purposes only. Cryptonary is not authorised or regulated by the Financial Conduct Authority (FCA) or any other financial regulatory body. Nothing in this publication constitutes a personal recommendation or advice to buy, sell, or hold any virtual asset. Virtual assets may lose their value in full or in part and are subject to extreme volatility. You can lose all invested amounts and do not benefit from any form of financial protection. Past performance does not indicate future results.

Recommended from Cryptonary