Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 43s

A Breakdown of (Micro)Strategy’s Latest Financial Instrument

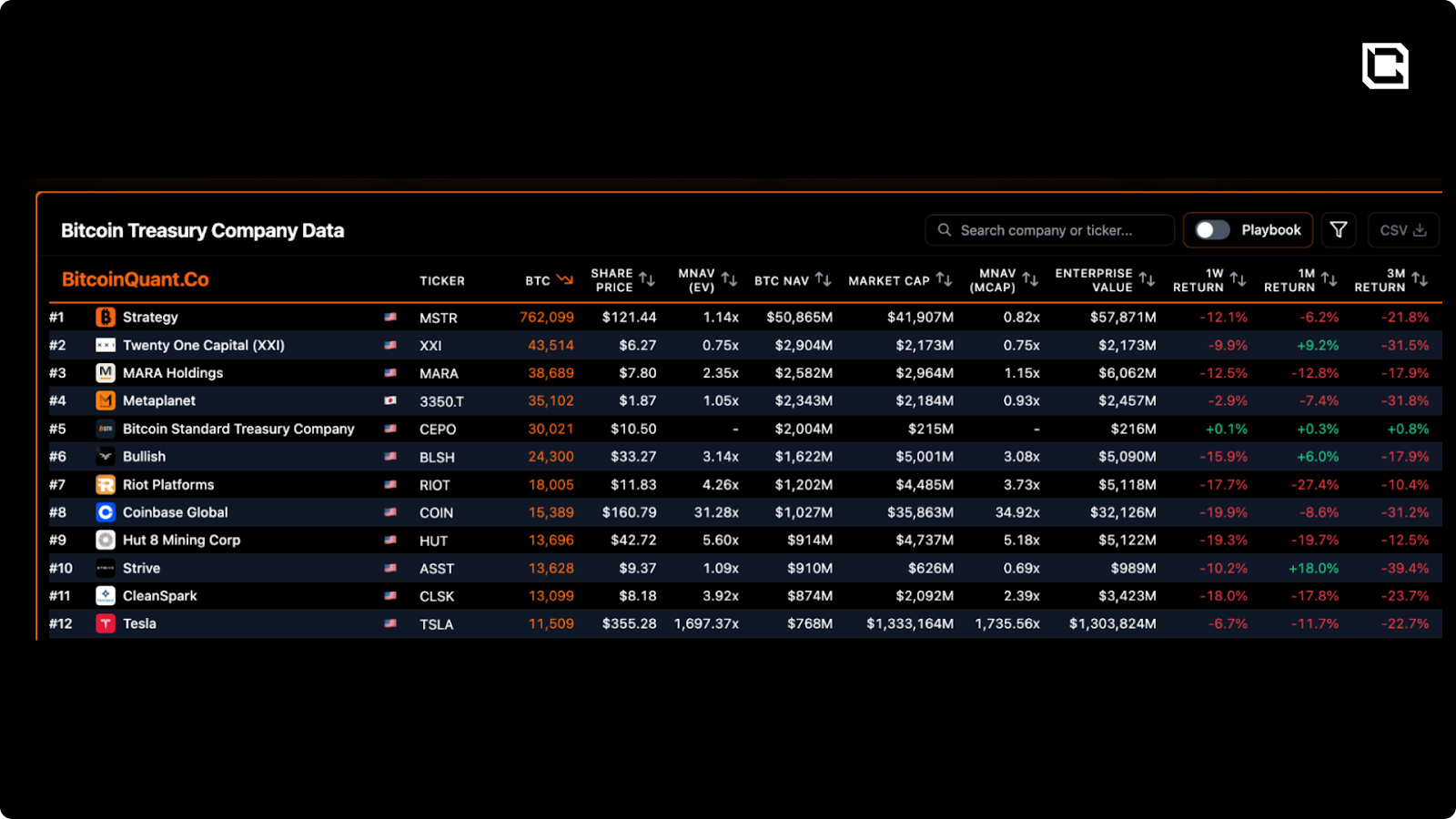

Strategy has built the most aggressive corporate Bitcoin treasury in history, holding 762,099 BTC worth over $50 billion. But the real story in 2026 is not Bitcoin itself. It is Stretch (STRC), the perpetual preferred stock instrument that has quietly become the primary engine for funding new purchases, even as the company's stock trades at a 17% discount to the value of its Bitcoin holdings and 73% below its all-time high.

In this report:

- What Strategy is and why it matters to Bitcoin

- How the full capital stack works

- Why STRC has overtaken converts and common equity as the most important funding tool

- Where the model becomes stressed, and what it means for Bitcoin’s market structure

Disclaimer: This is not financial or investment advice. You are responsible for any capital-related decisions you make, and only you are accountable for the results.

What is Strategy?

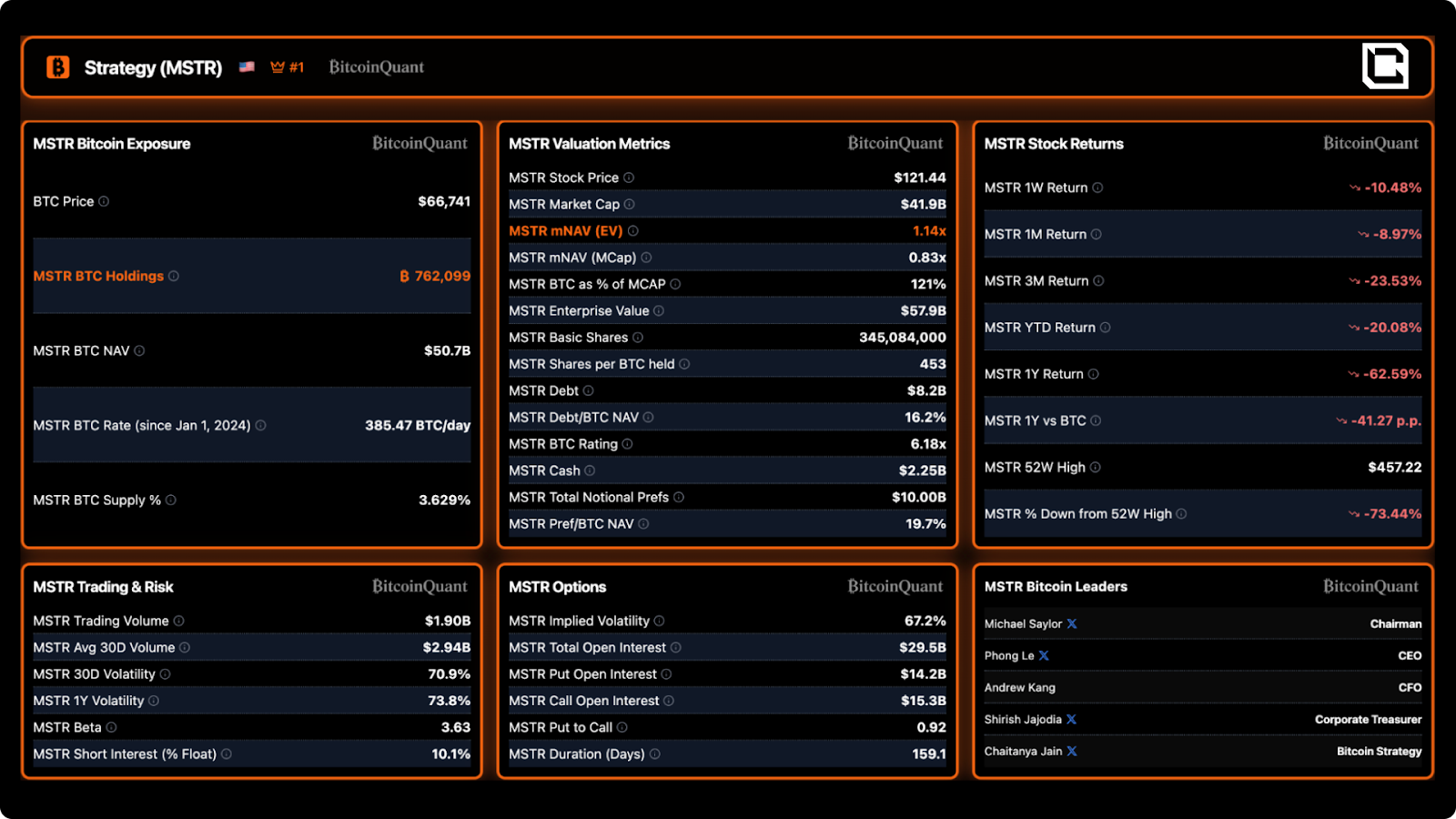

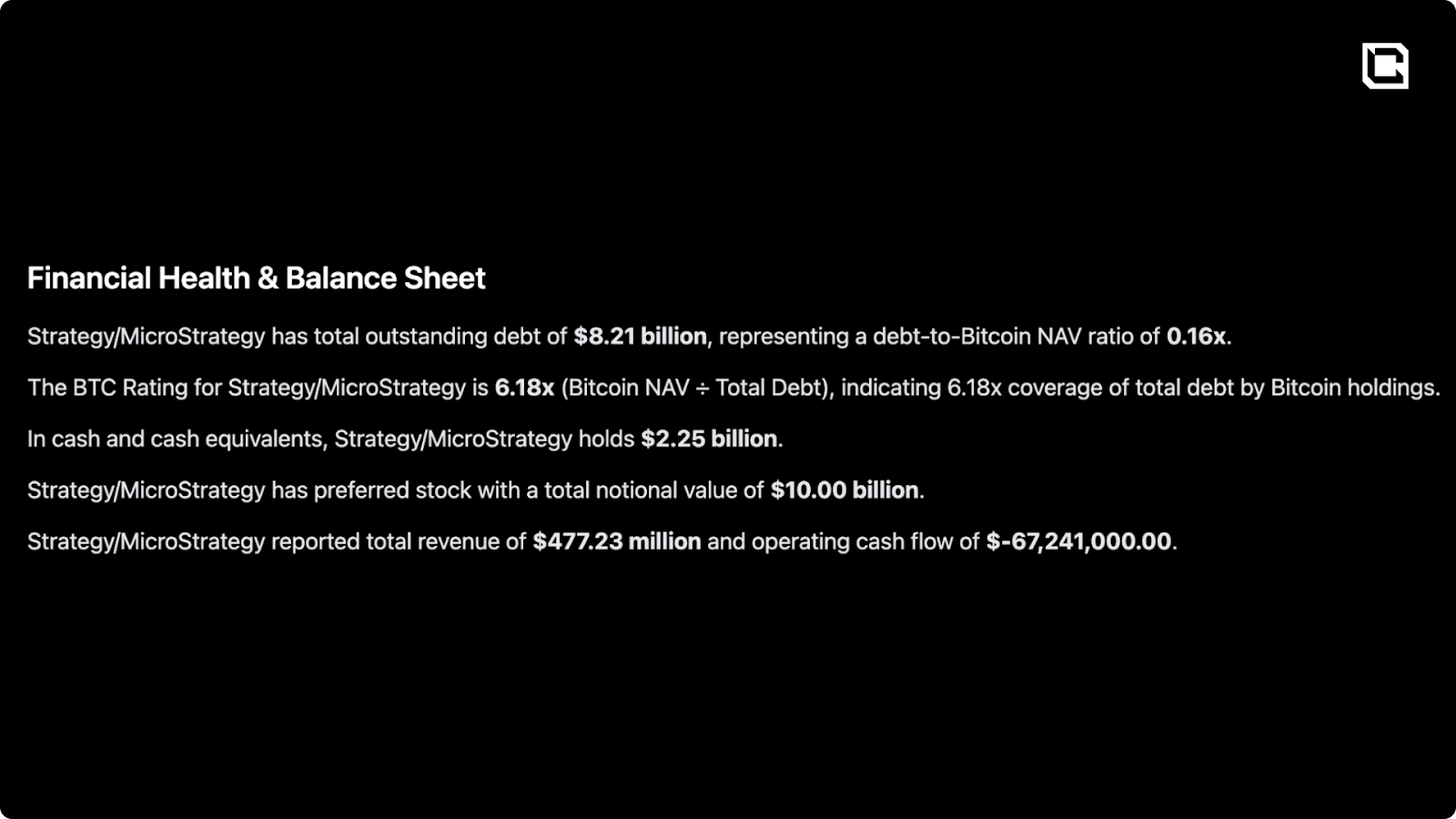

Strategy (formerly MicroStrategy) is a Bitcoin treasury company led by Executive Chairman Michael Saylor. The company's original software business still exists, generating roughly $477 million in annual revenue, but it is now a rounding error relative to the balance sheet. Strategy holds 762,099 BTC, acquired for a total of approximately $57.7 billion at an average cost of $75,694 per coin. That represents 3.63% of Bitcoin's total 21 million supply.The thesis is simple: Bitcoin is the best long-term store of value, and Strategy's job is to acquire as much of it as possible using every available capital markets tool. The company has transformed itself from a mid-cap software firm into what is effectively a publicly traded Bitcoin accumulation vehicle with a layered capital structure designed to attract different types of investors with different risk appetites.

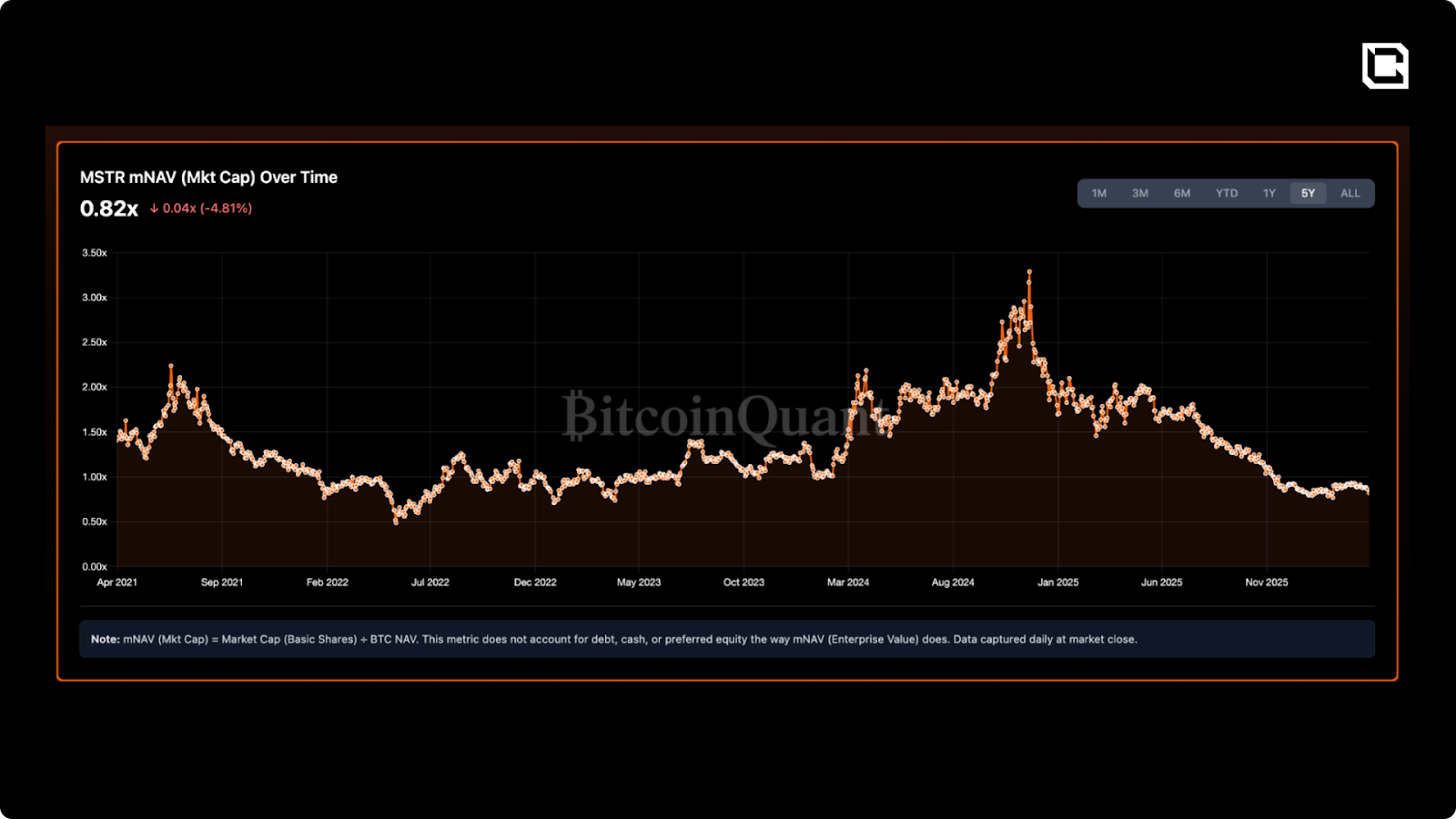

At a stock price of roughly $121, Strategy's market capitalization sits around $41.9 billion. Its Bitcoin holdings are worth approximately $50.7 billion at current prices. The company trades at an mNAV (market cap to Bitcoin NAV) of 0.82x, meaning the market currently values Strategy at less than the Bitcoin it holds. On an enterprise value basis, which accounts for debt and preferred equity, the mNAV is 1.14x. That gap between the two numbers tells you a lot about how the market is pricing the capital structure sitting on top of the Bitcoin.

The pace of accumulation has also become extraordinary. Since January 2024, Strategy has acquired Bitcoin at a rate of roughly 385 BTC per day. In March 2026 alone, it added more than 44,000 BTC across three major purchases. No other single corporate entity has built anything comparable.

The Capital Stack

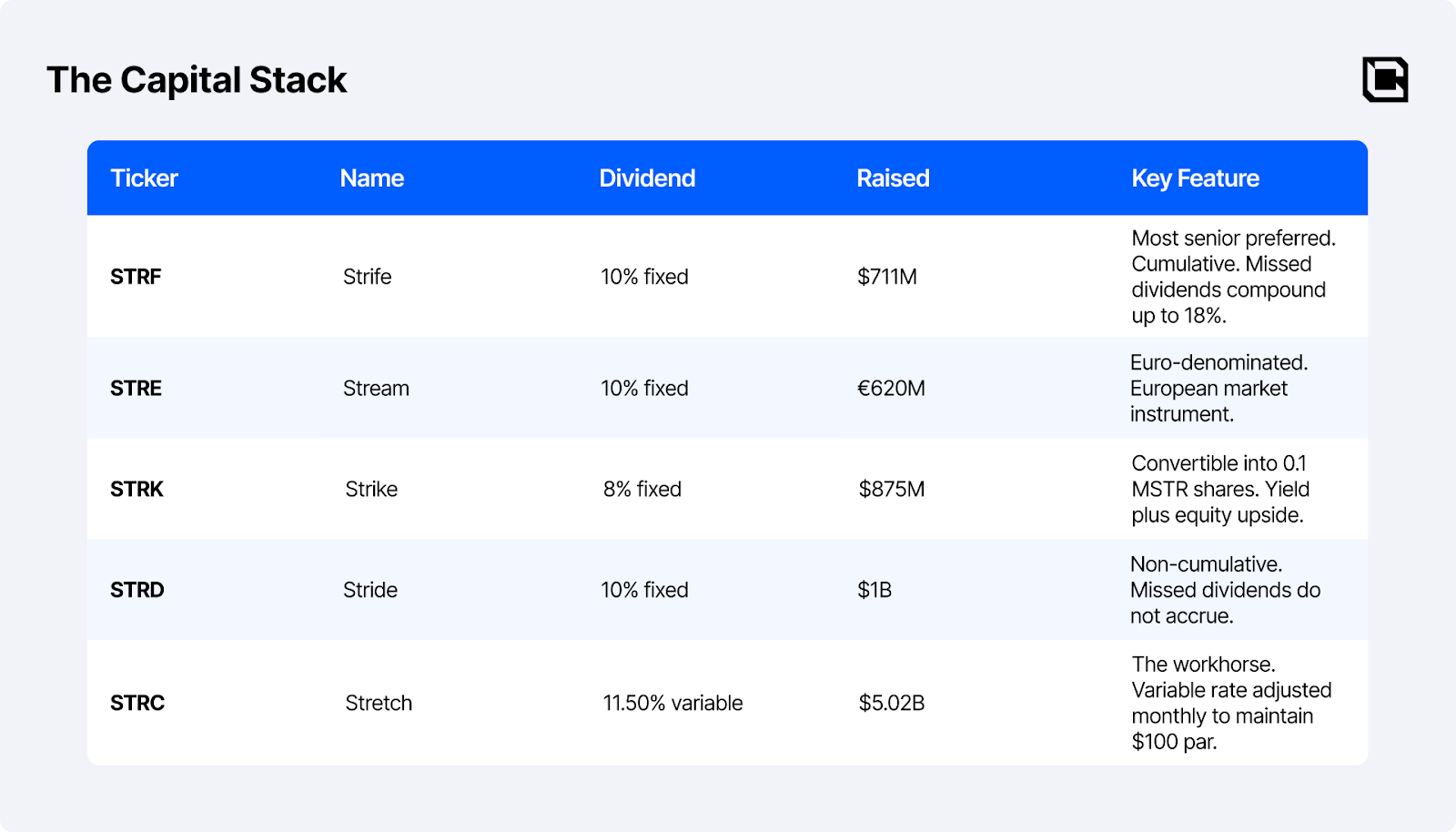

Strategy has built what amounts to a synthetic Bitcoin-backed yield curve. Each layer of the capital structure offers a different expression of Bitcoin exposure: the preferred instruments deliver low-volatility yield, while the common stock absorbs the excess risk and return, functioning as amplified Bitcoin.At the top of the seniority ladder sit the convertible senior notes. Strategy has approximately $8.2 billion in outstanding convertible debt, all carrying 0% interest rates. The two largest tranches are the $3 billion notes due December 2029 (convertible at $672.40 per share) and the $2 billion notes due March 2030 (convertible at $433.43 per share). There are no major maturities until 2028. With MSTR trading around $121, both conversion prices are deeply out of the money. Strategy has signaled plans to equitize roughly $6 billion of this debt over the next three to six years, converting bondholders into shareholders to reduce balance sheet pressure.

Below the debt sit five perpetual preferred stock instruments. The following table summarizes each, listed from most senior to most junior:

Common stock (MSTR) sits at the bottom with approximately 345 million shares outstanding, up from 76 million in 2020. The common absorbs all the excess volatility. With a beta of 3.63 and 30-day volatility of 70.9%, MSTR behaves like amplified Bitcoin. It is roughly the 250th largest US company by market cap but ranks among the top 15 by daily trading volume, averaging $2.94 billion per day over the past 30 days.

The total capital structure: $8.2 billion in convertible debt, $10.0 billion in preferred equity notional, $2.25 billion in cash, and approximately $50.7 billion in Bitcoin. The debt-to-BTC-NAV ratio is 16.2%. The preferred-to-BTC-NAV ratio is 19.7%. The BTC Rating (BTC NAV divided by total debt) is 6.18x, meaning Strategy's Bitcoin holdings cover its debt obligations more than six times over. Note that Strategy's own dashboard shows a 4.1x BTC Rating, which includes preferred equity in the denominator. The 6.18x figure covers debt obligations only.

STRC: The Engine Powering the Machine

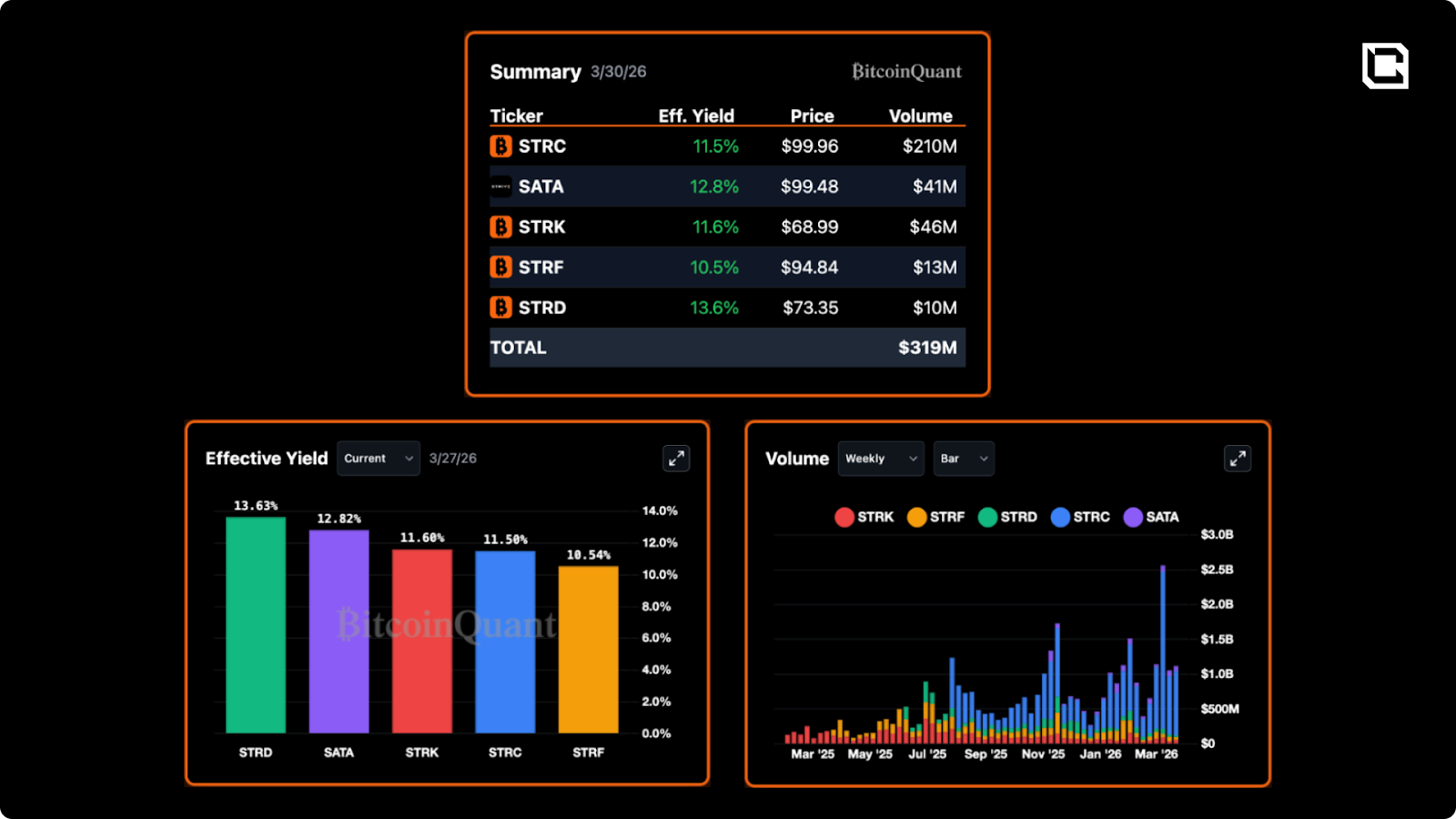

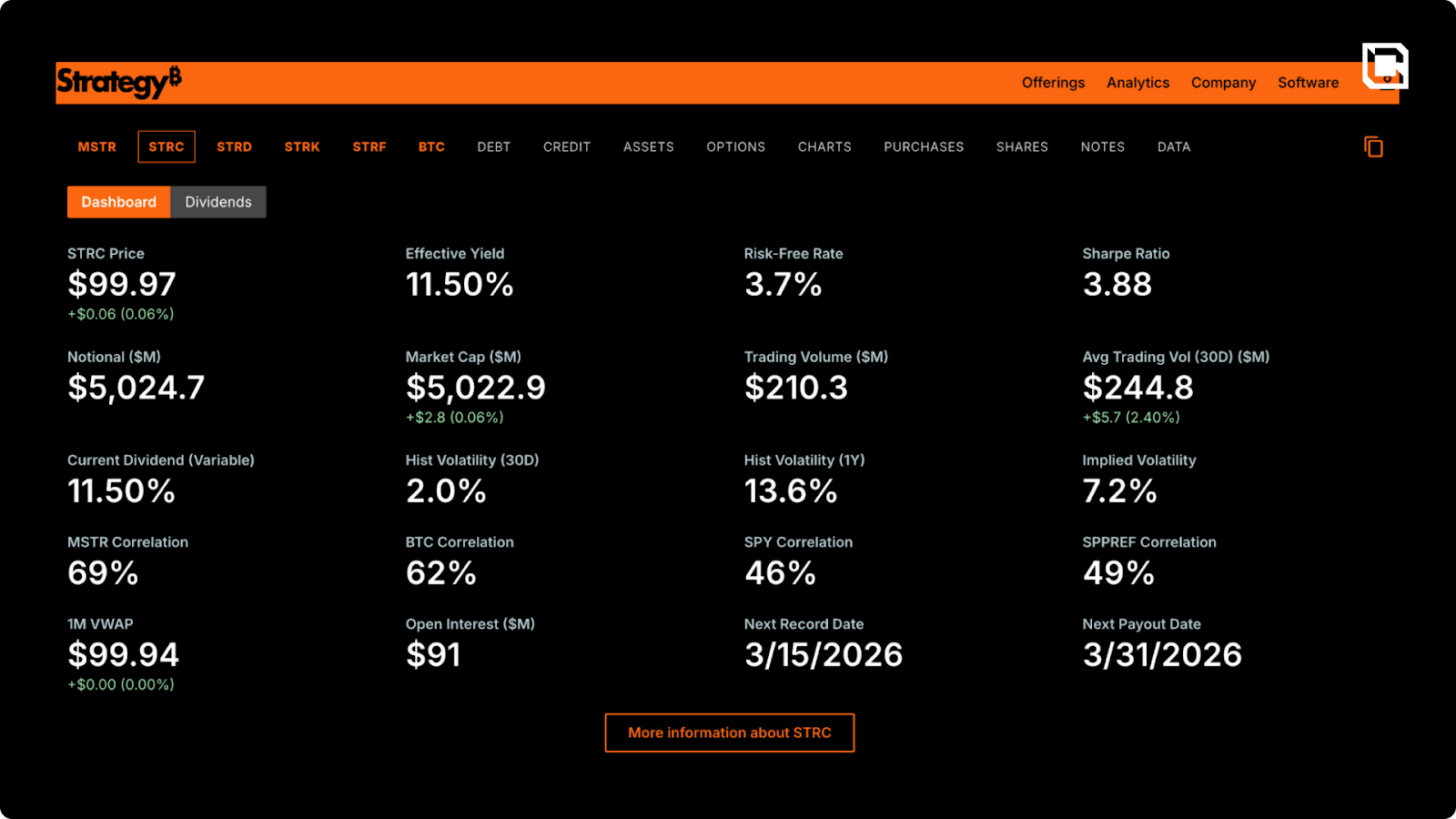

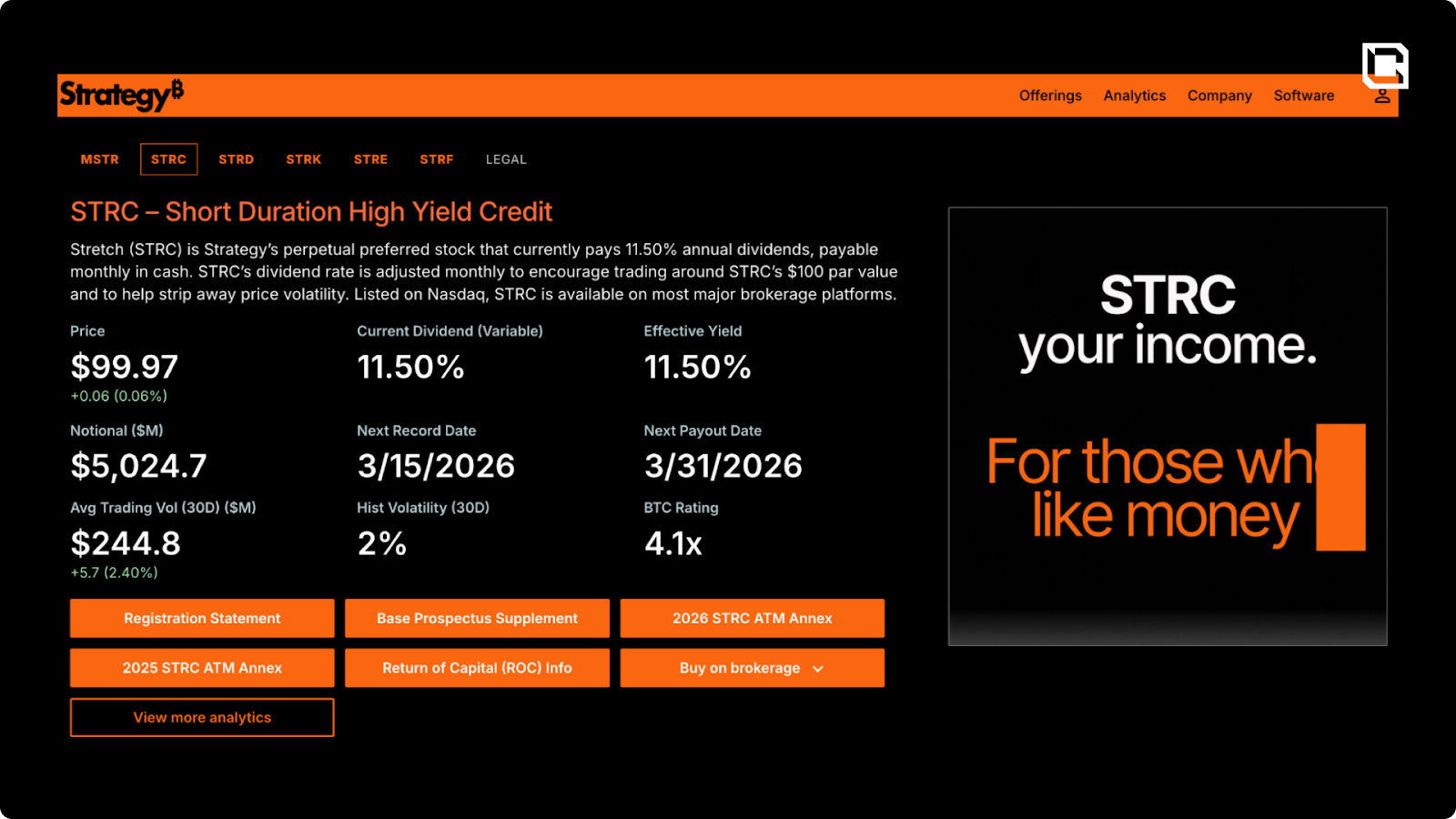

Stretch launched in July 2025 via a $4.2 billion at-the-market program. The concept was straightforward: create a perpetual preferred stock that behaves like a high-yield savings account backed by Bitcoin. It pays a variable dividend (currently 11.50%, up from 9% at launch), trades on Nasdaq with full retail and institutional access, and is designed to hold close to its $100 par value with minimal price volatility.

The product targets a very specific pool of capital. STRC is not designed for the investor who wants raw Bitcoin beta. It is designed for pools of capital that want yield, liquidity, and structure, but cannot or will not buy Bitcoin directly. That includes insurance companies, pension funds, endowments, and more conservative asset managers operating under mandate or policy constraints. For those investors, STRC offers exposure to a Bitcoin-linked capital structure without requiring direct ownership of Bitcoin itself.

That is what makes the product strategically important. Strategy is not just raising money from crypto-native speculators. It is attempting to tap into the much larger global fixed-income universe, estimated at roughly $200 trillion to $300 trillion.

For context on what makes STRC different from traditional preferred equity: the largest banks on the planet, JP Morgan, Wells Fargo, Bank of America, issue preferred equity that pays roughly 6% and trades with minimal daily volume. STRC pays 11.50% and averages $244.8 million in daily trading volume with only 2% 30-day price volatility and a Sharpe ratio of 3.88. That combination of high yield, high liquidity, and low volatility is why the product has attracted over $5 billion in notional in eight months.

How it Funds Bitcoin Purchases

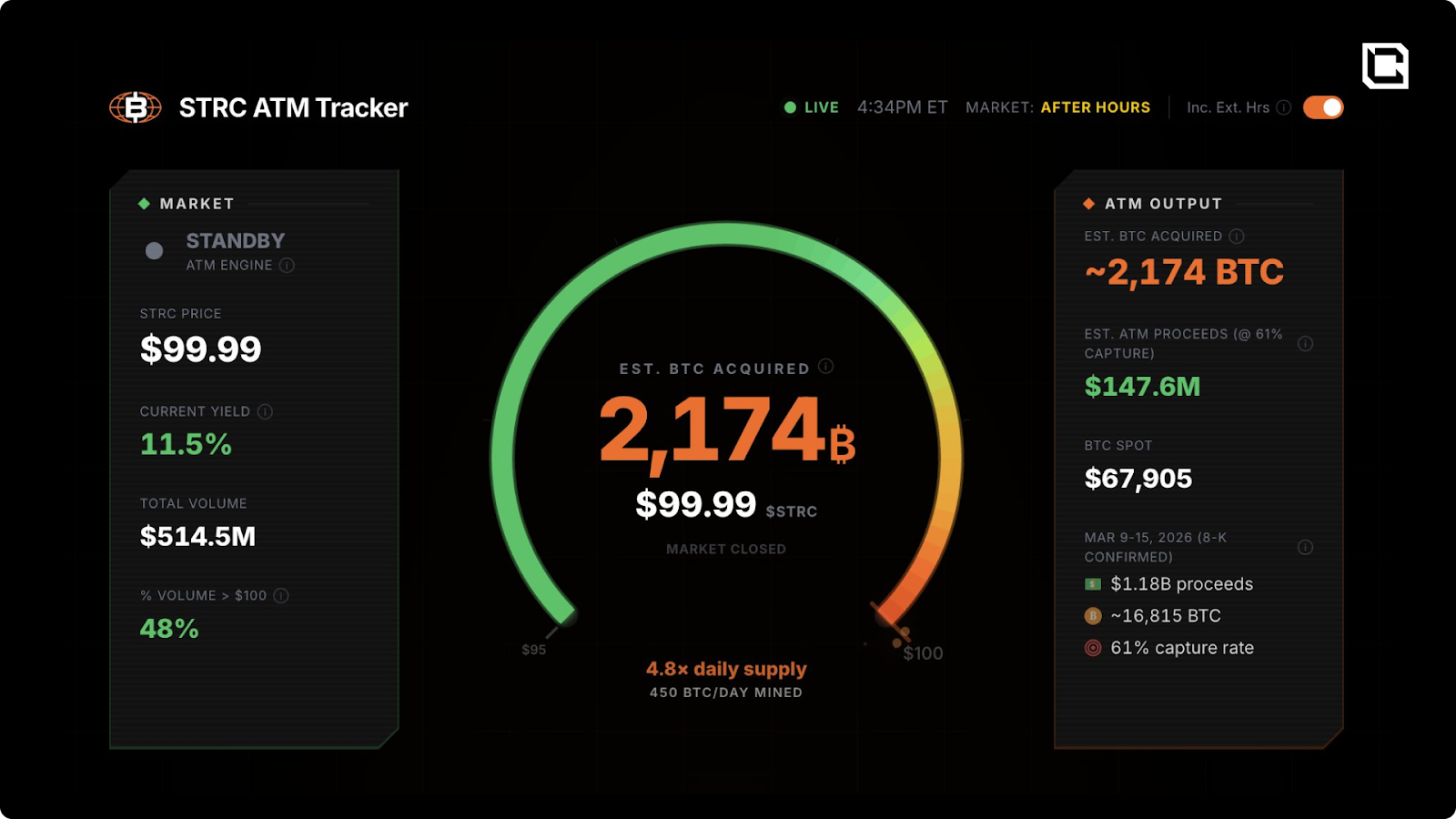

The mechanics are direct. Strategy sells STRC shares into the open market through its ATM program whenever the price is at or above $100 par. Every dollar raised goes toward Bitcoin acquisition and working capital. The company has publicly stated it will not sell STRC below par. Market participants have observed that historically, roughly 50% of STRC volume trading above $100 represents new issuance flowing into Strategy's treasury.Once the cash comes in, Strategy deploys it into Bitcoin purchases, likely through OTC desks or prime brokers to minimize market impact on a $1.3 trillion asset. The company reports its purchases weekly in SEC filings, with average prices listed as inclusive of fees and expenses.

That means the reported cost basis bakes in broker fees, OTC spreads, and transaction costs on top of the actual execution price. When the reported average looks slightly above the spot price at the time of the Monday announcement, that gap is mostly explained by the blended execution across the full seven-day window plus those embedded costs. For the March 9 to 15 purchase of 22,337 BTC at $70,194, the average price was actually slightly below the volume-weighted average for the period.

There is a front-running question worth acknowledging. Saylor's weekly cadence is predictable: buy throughout the week, post a signal on X Sunday evening, file the 8-K Monday morning. The market knows capital is flowing in. Traders could theoretically position ahead of the expected demand. OTC execution reduces this risk, but does not eliminate it entirely. It is an inherent friction of running the most visible Bitcoin accumulation program in the world.

The shift to STRC as the primary funding tool became explicit the week of March 9 to 15, 2026. Strategy purchased 22,337 BTC for $1.57 billion. Of that, $1.18 billion came from STRC issuance, far exceeding the $396 million raised through common stock sales. That was the first time in Strategy's history that preferred equity outpaced common stock as the dominant funding source.

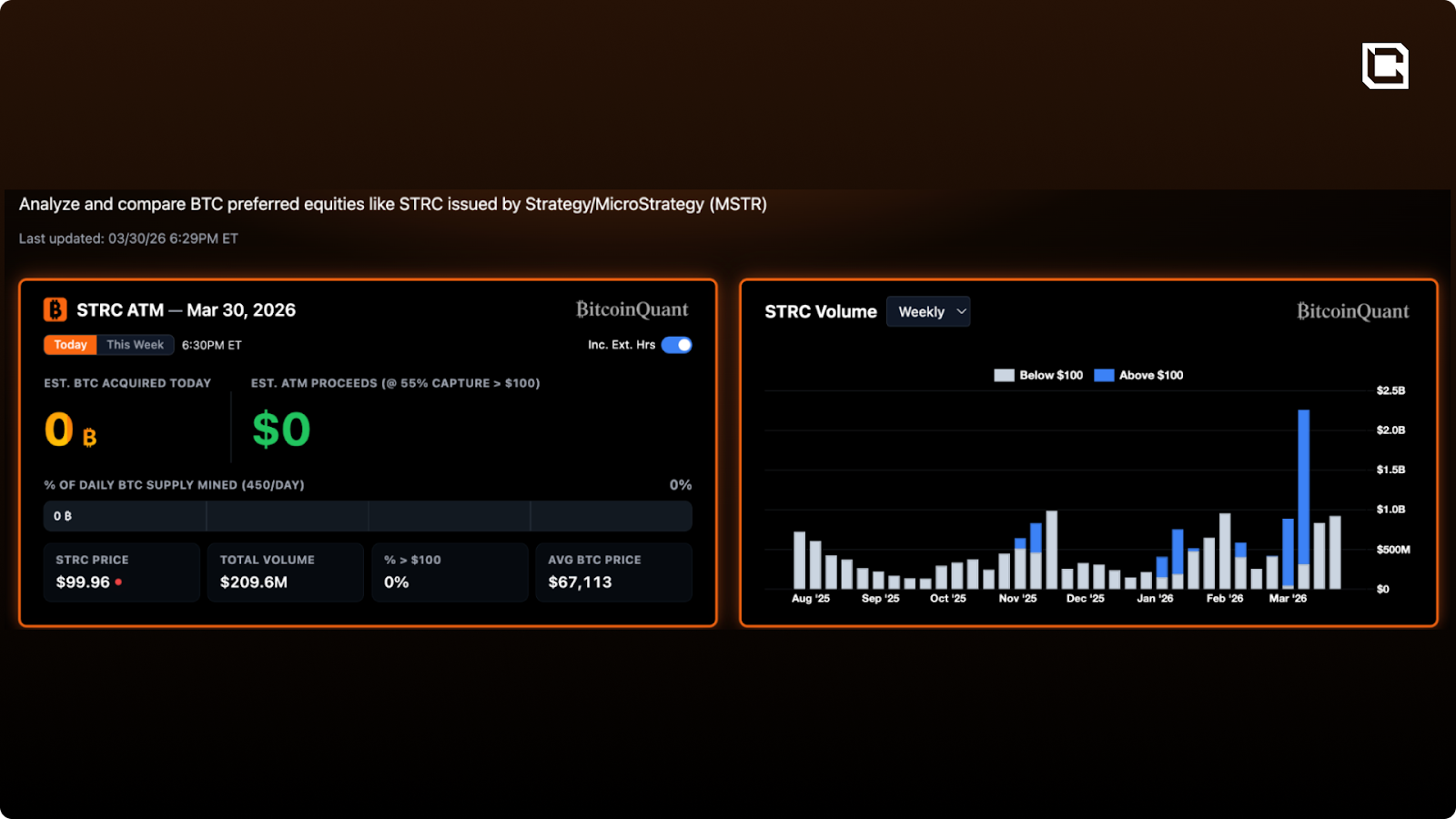

Strategy maintained a streak of thirteen consecutive weekly Bitcoin purchases from late December through March 22, accumulating 90,831 BTC in the process. That streak ended the week of March 23 to 29, when the company confirmed it made no purchases. Saylor's usual Sunday signal post was replaced with STRC marketing. Whether this was a tactical pause related to STRC pricing pressure after the ex-dividend date, a brief capital-raising gap, or something else entirely remains unclear. But the machine was not buying for the first time in over three months.

Why the shift? The convertible debt window is effectively closed. With MSTR trading at $121, well below the conversion prices of $433 and $672 on the outstanding notes, issuing new converts at attractive terms is not realistic. Meanwhile, issuing common stock at an mNAV below 1x is mechanically dilutive to BTC per share. Every share sold below NAV reduces existing shareholders' proportional claim on the Bitcoin treasury. Strategy is still doing it, accepting the short-term dilution to maintain accumulation pace, but it is no longer the preferred tool.

STRC solves both problems. It is not convertible, so it does not directly dilute common equity. It has no maturity date, so there is no refinancing risk. And because it sits above common equity in the capital structure, credit-sensitive investors are willing to accept the yield in exchange for seniority over MSTR holders.

On March 23, 2026, Strategy announced a new $42 billion ATM program: $21 billion in common stock and $21 billion in STRC. That is the next phase of the accumulation playbook.

The Dividend Treadmill

This is the cost of running the machine. STRC's variable dividend has been increased seven times since launch: from 9.00% in July 2025 to 9.50%, 10.00%, 10.25%, 10.50%, 10.75%, 11.00%, and now 11.50% as of March 2026. Each 25-basis-point increase was made to keep STRC trading near its $100 par value so that Strategy can continue issuing new shares through the ATM.After ex-dividend dates, STRC typically dips below par as holders capture the dividend and some sell. The company then has to wait for the price to recover before it can resume issuance. Following the March 15 ex-dividend, STRC returned to $100 par within nine trading days, slightly faster than its historical average of ten days.

The total annual dividend obligation across all preferred instruments now exceeds $1 billion. Strategy holds $2.25 billion in cash, providing roughly 24 to 32 months of dividend coverage depending on the calculation method. Behind that cash buffer sits $50.7 billion in Bitcoin, representing approximately 17 years of dividend coverage at current prices.

The question is how sustainable the treadmill is. Every hike makes the next issuance more expensive. At 11.50%, STRC already yields nearly double what comparable bank-issued preferred instruments pay. If the price continues to drift below par between ex-dividend dates, the yield will need to keep climbing. At some point, the cost of funding begins to weigh on the overall value proposition for common shareholders.

That said, the math still works at current levels. Per the company's own analysis, Strategy needs Bitcoin to appreciate at roughly 1.8% annually to cover dividend obligations indefinitely. The US M2 money supply has grown at approximately 6.7% compounded annually since 1970. Even a modest Bitcoin beta to monetary expansion would comfortably exceed the required growth rate.

Can It Break?

Strategy's balance sheet is designed to survive deep drawdowns. The debt-only BTC Rating of 6.18x means Bitcoin would need to fall roughly 84% from current levels before debt obligations exceed the value of the Bitcoin holdings. Including preferred equity, the coverage ratio drops to 4.1x, which still implies substantial headroom. The company has stated that even at $8,000 BTC, reserves would still cover liabilities. But the more realistic stress scenarios are not about insolvency. They are about the ability to keep the machine running.- Scenario 1: Prolonged mNAV discount. If MSTR continues to trade below NAV, common stock issuance is dilutive, STRC issuance becomes the only effective tool, and the dividend treadmill accelerates. The company can still accumulate Bitcoin, but at an increasingly expensive cost of capital.

- Scenario 2: STRC pricing pressure. If Bitcoin enters a sustained bear market and STRC consistently trades below par despite dividend hikes, the ATM program stalls. Strategy cannot sell STRC below $100. The cash buffer buys time (two-plus years at current levels), but the accumulation engine stops.

- Scenario 3: Dividend pause. In extreme distress, Strategy could pause preferred dividends. On STRF, unpaid dividends compound at escalating rates up to 18%. On STRD, unpaid dividends are simply lost (non-cumulative). STRC sits in between: dividends are cumulative, meaning missed payments accrue and are still owed. Critically, unpaid STRC dividends compound monthly at the prevailing variable rate (currently 11.50%), so a missed payment does not just defer the cost, it increases it. Strategy is also blocked from paying dividends on anything junior to STRC (including common stock) until all STRC arrears are paid in full, and it cannot reduce the STRC dividend rate until those arrears are cleared. A dividend pause would likely trigger a sharp selloff in the preferred instruments and raise serious questions about the sustainability of the model. This is a low-probability scenario, but it is worth understanding.

- Scenario 4: Forced Bitcoin sales. This is the true tail risk. If all other capital-raising channels close and cash reserves deplete, Strategy would need to sell Bitcoin to meet obligations. Given the company's holdings represent 3.63% of total supply, any forced selling would likely be visible to the market and could create a negative feedback loop. Strategy has explicitly stated it does not intend to sell Bitcoin.

What Does This Mean for Bitcoin?

Strategy now holds 762,099 BTC, or 3.63% of Bitcoin's total 21 million supply. Across all 151 publicly traded Bitcoin treasury companies tracked by BitcoinQuant, total holdings are 1,165,280 BTC, representing 5.55% of supply. Strategy alone accounts for roughly 65% of all corporate Bitcoin holdings.The STRC machine has created something that did not exist in previous bear markets: a persistent, structural bid for Bitcoin funded by capital that would never have entered the Bitcoin market directly. Every dollar raised through STRC issuance is converted into a Bitcoin purchase. At the current pace, Strategy is adding roughly 385 BTC per day.

The second-largest publicly traded Bitcoin holder is Twenty One Capital (XXI) with 43,514 BTC. Strategy holds over 17 times more. MARA Holdings sits third at 38,689 BTC, and Metaplanet fourth at 35,102 BTC. The gap is enormous.

This concentration creates both a structural demand floor and a tail risk. On the demand side, Strategy's ongoing accumulation absorbs supply at a rate that few other market participants can match. On the risk side, if Strategy were ever forced to sell, the impact would be significant. But that risk is mitigated by the capital structure specifically designed to prevent forced selling: perpetual instruments with no maturity, a $2.25 billion cash buffer, and 4.1x coverage when including all obligations.

The broader implication is that Bitcoin's market structure is changing. The plumbing now includes a perpetual, yield-funded bid from capital pools that previously had zero Bitcoin exposure. Insurance company balance sheets, pension fund allocations, and conservative fixed-income portfolios are entering the Bitcoin ecosystem through instruments like STRC without ever touching a satoshi directly. That is new. And it is structural, not cyclical.

Cryptonary's Take

What Strategy has built is genuinely unprecedented in financial markets. They have taken a volatile, 24/7, globally liquid asset and layered a full capital structure on top of it: convertible debt, five tiers of preferred equity, and a common stock that functions as leveraged Bitcoin. The result is a machine that converts conservative capital into Bitcoin demand.STRC is the most important piece right now. The convertible debt playbook worked brilliantly in the bull market of 2024 and early 2025, but it has limitations: maturity dates, refinancing risk, and covenants. STRC has none of those. It is perpetual. It sits junior to debt. And it has attracted $5 billion in notional in eight months, trading at volumes that dwarf everything else in the preferred equity market.

The risk is the treadmill. Seven dividend hikes in eight months tells you that keeping STRC at par is not effortless. Every increase raises the annual cost of the machine. At $1 billion-plus in annual dividend obligations and growing, the margin for error narrows. If Bitcoin enters a prolonged decline and the ATM stalls, the cash buffer buys time but does not buy indefinitely.

The skeptic's question is obvious: is this just an elaborate Ponzi? New money from STRC buyers funds the purchases, dividends are not covered by operating revenue, and the machine requires continuous capital inflows to sustain itself. The comparison is understandable but ultimately wrong. A Ponzi has no real assets behind it. Strategy has 762,099 BTC sitting verifiably on-chain, worth roughly $50 billion. Every dollar of debt, preferred equity, and Bitcoin is disclosed in SEC filings. STRC holders can exit at any time on the open market. There is no fraud and no opacity. What Strategy is running is not a Ponzi. It is a leveraged, reflexive bet on Bitcoin with an expensive cost of capital. But leverage has its own risks, and the need for continuous market access to sustain itself is the single most important thing to understand about this model.

We are not recommending MSTR, STRC, or any Strategy instrument as a trade. What we are saying is that understanding this structure is essential for anyone with a view on Bitcoin. Strategy is adding roughly 385 BTC per day. It holds 3.63% of total supply. And the instrument funding those purchases is tapping a capital pool that is orders of magnitude larger than the entire Bitcoin market.

Whether you view this as financial genius or an elaborate house of cards probably depends on your conviction in Bitcoin's long-term trajectory. If Bitcoin grows at even a fraction of the historical M2 money supply expansion rate, the math works and the dividends get paid. If Bitcoin enters a multi-year decline with no recovery, the model comes under real pressure, though the 4.1x BTC Rating (including preferred obligations) and $2.25 billion cash reserve suggest it would take a truly extreme scenario to break it.

The bottom line: the plumbing of Bitcoin has changed. STRC is the clearest example of how traditional capital markets infrastructure is being built around Bitcoin, and why this cycle's demand dynamics look fundamentally different from anything that came before. This is worth paying attention to.

Cryptonary, OUT!

Recommended from Cryptonary