Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 43s

The Clarity Act and the Future of Crypto Markets

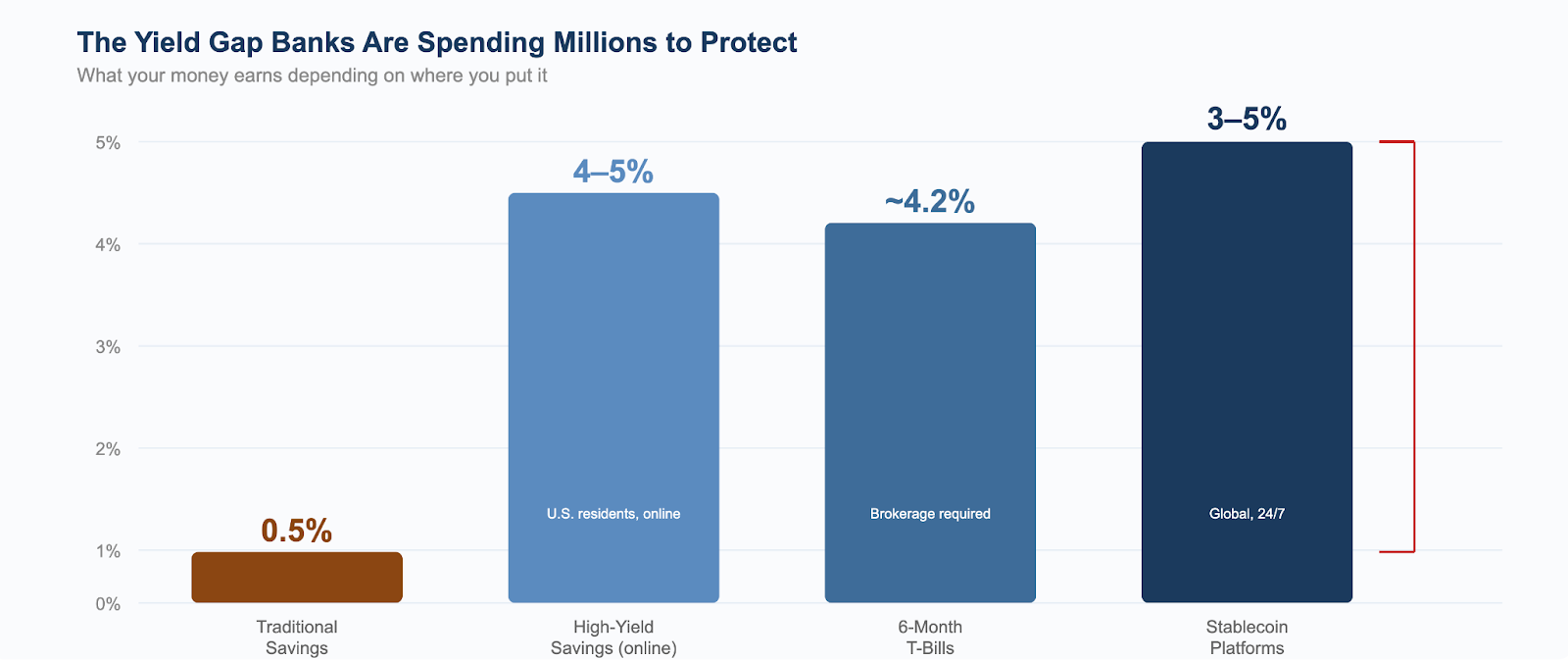

Your savings account pays 0.5%. A stablecoin platform pays 4%. That spread has sparked a $250 million lobbying war and stalled the most consequential crypto bill in U.S. history. The midterm clock is ticking, and macro has already shown it does not care about Washington. This report explains what the CLARITY Act changes, what it does not, and what that means for your portfolio.

In this report:

- What the CLARITY Act actually changes and what it does not

- The stablecoin yield war and why banks are spending tens of millions to kill it

- Key players, legislative timeline, and the real deadlines

- Scenario analysis and the implementation gap between passage and impact

- Price action: honest assessment grounded in macro reality

Disclaimer: This is not financial or investment advice. You are responsible for any capital-related decisions you make, and only you are accountable for the results.

The Big Picture

For the first time in its history, the United States Congress is on the verge of telling the world what crypto actually is. The CLARITY Act is the vehicle, and it has gotten further than any digital asset legislation before it, passing the House with 294 votes, earning White House support, and securing genuine bipartisan backing. And yet, despite all of that momentum, the bill is stuck.The Digital Asset Market Clarity Act of 2025 is the most significant attempt by the United States Congress to establish a comprehensive federal regulatory framework for digital assets. The bill was introduced on May 29, 2025, by House Financial Services Committee Chairman French Hill, a Republican representing Arkansas, and passed the House of Representatives on July 17, 2025, with a bipartisan vote of 294 to 134.

The legislation draws a statutory line between securities jurisdiction under the SEC and commodities jurisdiction under the CFTC, creates tailored registration pathways for crypto intermediaries, establishes an exemption for decentralized finance protocols, and mandates coordination between the two agencies. It is designed to work alongside the GENIUS Act, which Congress passed in July 2025 to govern stablecoin issuance.

The bill is stuck because the traditional banking industry and the crypto industry are locked in a fight over whether stablecoin platforms should be allowed to pay yield to their customers. Between the two sides, more than $250 million in lobbying and political spending has been deployed, and three rounds of White House-brokered negotiations have failed to produce a deal.

As of late February 2026, the Senate Banking Committee has postponed its scheduled markup indefinitely after Coinbase and other industry participants publicly withdrew support over revised provisions restricting stablecoin yield. The real hard deadline is the November 2026 midterm elections. If the bill does not pass before midterms, a shift in congressional composition could stall or reverse the effort entirely.

The CLARITY Act is a structural regulatory unlock with multi-year implications for how crypto is classified, traded, and custodied in the United States, and it removes a genuine headwind that has kept institutional capital on the sidelines.

Key Provisions of the CLARITY Act

Jurisdictional Delineation

The foundational achievement of the bill is its attempt to resolve the longstanding jurisdictional conflict between the SEC and CFTC. For years, both agencies have asserted expansive claims over crypto asset oversight, resulting in contradictory enforcement actions, divergent classification standards, and an environment the industry has characterized as regulation by enforcement.The CLARITY Act introduces formal statutory definitions for “digital commodity,” “investment contract asset,” and “blockchain” directly into the Securities Act of 1933, the Securities Exchange Act of 1934, and the Commodity Exchange Act.

Digital assets that have achieved sufficient decentralization and are not sold as part of an investment contract are classified as digital commodities under CFTC oversight. Assets sold through fundraising mechanisms resembling securities offerings remain under SEC purview. The bill mandates joint rulemaking and coordination between the agencies on cross-jurisdictional matters including delisting decisions.

Registration Framework

The CLARITY Act creates purpose-built registration categories for digital asset exchanges, brokers, dealers, and custodians. Rather than requiring crypto intermediaries to retrofit themselves into legacy securities or commodities frameworks, the bill establishes tailored compliance pathways with expedited registration provisions and a provisional status mechanism.This allows firms to operate lawfully while full applications are processed. The legislation also includes protections for non-controlling blockchain developers, treating decentralized governance system participants as separate legal persons from the protocol itself unless they are under common control or acting in concert.

DeFi Exemption and Anti-CBDC Provisions

Section 309 provides an exemption for certain decentralized finance activities from the most onerous regulatory requirements. This represents the first statutory recognition that decentralized protocols occupy a distinct regulatory category from centralized intermediaries. In practical terms, it means that truly decentralized protocols would not need to register as exchanges or broker-dealers, which is a significant departure from the SEC’s previous stance under the prior administration.Separately, the CLARITY Act includes the Anti-CBDC Surveillance State Act as a companion provision, which would prohibit the Federal Reserve from researching, designing, or issuing a central bank digital currency without explicit congressional authorization. The House passed this provision 219 to 210 on July 17, 2025.

Relationship with the GENIUS Act

The CLARITY Act does not exist in isolation. It is designed to work alongside the GENIUS Act, which governs stablecoin issuance and includes provisions allowing national trust banks to issue payment stablecoins under prudential supervision. The GENIUS Act prohibits the payment of interest on stablecoins by issuers but remains silent on rewards-based compensation.That ambiguity is exactly what has become the central point of contention in the CLARITY Act negotiations. The banking lobby is pushing to use CLARITY’s Section 404 to close the rewards loophole that the GENIUS Act left open. Any institutional analysis of the regulatory landscape must treat these two bills as a package deal rather than independent legislative efforts.

The Stablecoin Yield War

The single most consequential unresolved issue is whether stablecoin issuers or platforms may pay yield to holders. The Senate Banking Committee’s January 12, 2026, draft included Section 404, which would prohibit digital asset service providers from offering interest or yield to users for simply holding stablecoin balances while allowing activity-linked or transaction-based incentives. Violations would carry penalties of $500,000 per offense per day, enforced jointly by the SEC, Treasury, and CFTC.

Comparison table of yields in the market

This provision has become the central battleground between the traditional banking sector and the crypto industry. Banks are fighting to protect their deposit base and the interest income it generates. Crypto firms are fighting to preserve the ability to offer a superior product to consumers. The White House’s Crypto Policy Council has brokered three negotiation sessions between the two sides (February 2, 10, and 19, 2026), with Coinbase, Circle, Ripple, Crypto.com, and a16z representing the crypto industry, and the Bank Policy Institute and American Bankers Association representing banks.No final agreement has been reached. The emerging compromise framework would distinguish between idle yield (banned) and activity-based rewards (potentially permitted), but the specific language remains unresolved.

The Systemic Argument: A Fair Hearing

It is tempting to frame the banking lobby’s position as pure regulatory capture, and there is substantial truth to that framing. Banks could compete on product quality and yield rather than lobbying to legislate their competition out of existence.However, the systemic argument is not entirely without merit. If yield-bearing stablecoins scale rapidly and attract large deposit outflows from commercial banks, lending capacity contracts. Banks fund loans through deposits. A sudden, large-scale shift of deposits into stablecoin products does not just hurt bank profitability; it reduces the pool of capital available for consumer and business lending.

Regional and community banks, which are more deposit-dependent than large money-center banks, would feel this disproportionately. This does not mean the yield ban is the right policy response, but institutional readers should understand that the systemic argument has non-zero substance even if the primary motivation behind the lobbying is competitive self-interest.

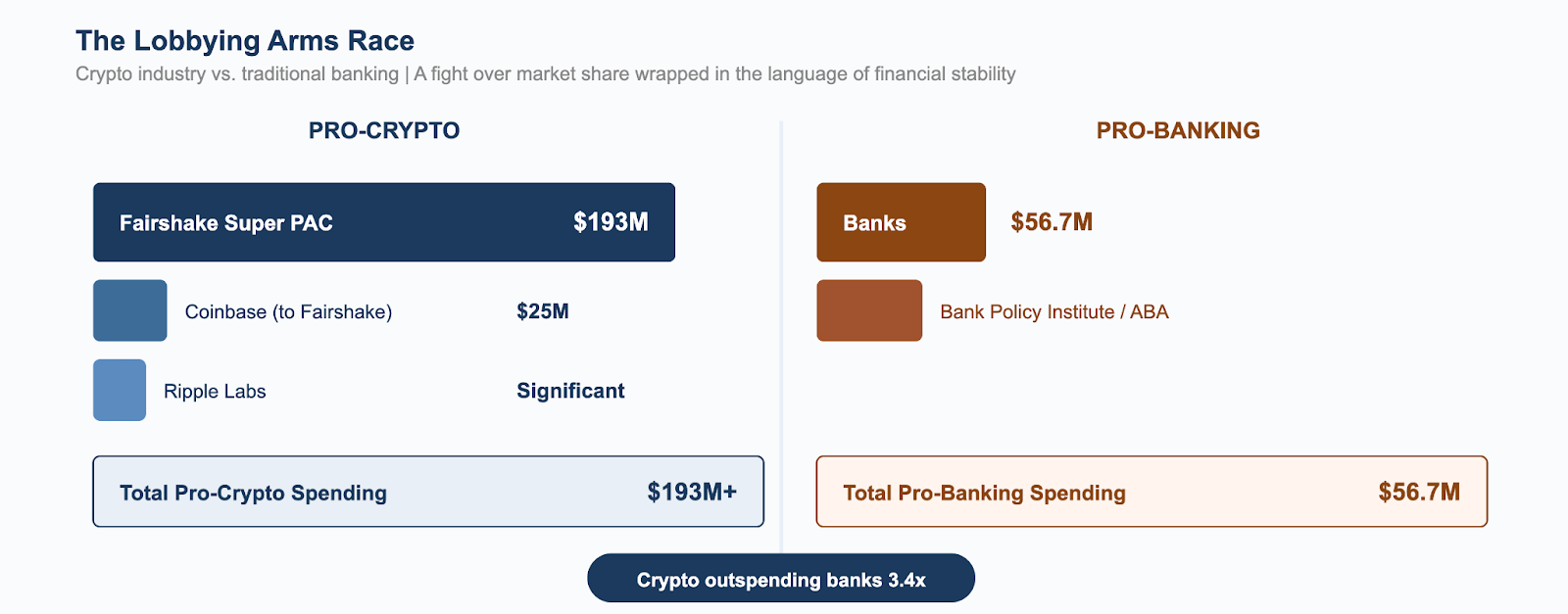

The Lobbying Arms Race

Thus, the CLARITY Act has triggered one of the most expensive lobbying campaigns in recent financial regulatory history. On the crypto side, the Fairshake Super PAC announced $193 million in cash on hand as of January 28, 2026, with Coinbase contributing $25 million and Ripple Labs contributing a significant additional sum.On the banking side, commercial banks spent $56.7 million on lobbying in 2025 according to OpenSecrets data. While not all of that spend was CLARITY-specific, a substantial portion was directed at shaping stablecoin yield provisions. To put those numbers in context, U.S. commercial bank deposits totaled approximately $18.8 trillion as of early 2026, which means the banking lobby is spending roughly 0.0003% of its deposit base to protect the entire thing. That is an extraordinary return on investment if it works, and it explains why the spend seems modest relative to what the crypto side has deployed. The scale of spending on both sides reveals the true stakes: this is fundamentally a fight over market share wrapped in the language of financial stability.

Lobbying data: Crypto vs Banks

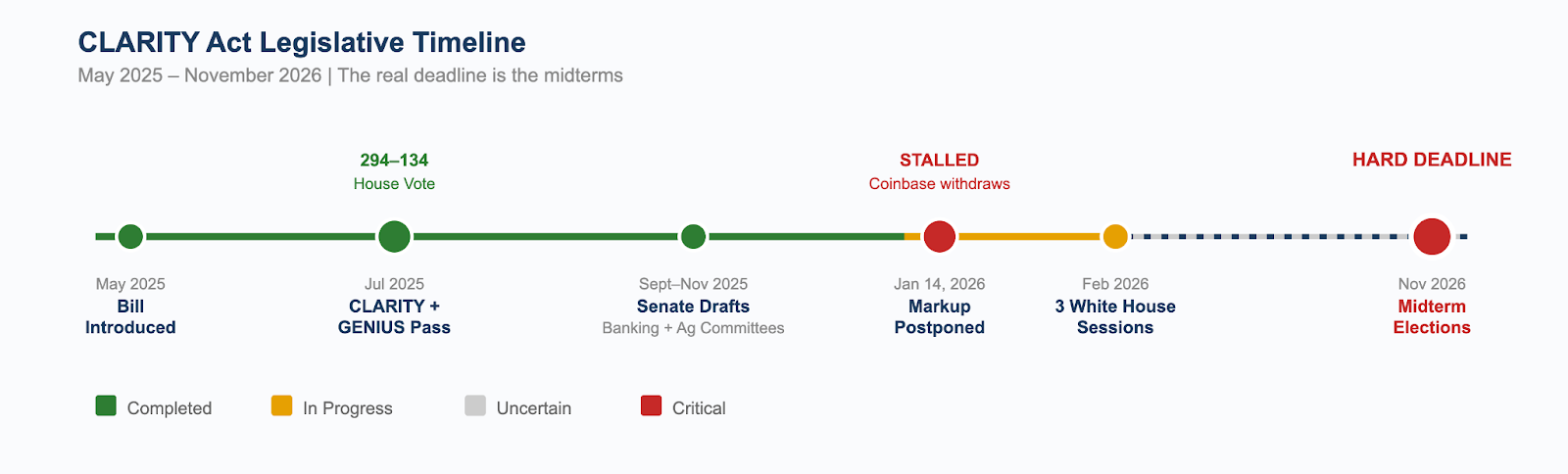

Legislative Timeline

The CLARITY Act was introduced on May 29, 2025. During “Crypto Week” in July, the House passed both the CLARITY Act (294 to 134) and the CBDC Anti-Surveillance State Act (219 to 210). The GENIUS Act also passed Congress that month, establishing the regulatory foundation for stablecoin issuance. The White House issued a Statement of Administration Policy supporting CLARITY’s goals.Through the fall, the Senate developed its own versions. The Senate Banking Committee released a 182-page discussion draft in September, followed by a 278-page revision. The Senate Agriculture Committee released a separate draft under Sen. Boozman and Sen. Booker in November. Twelve Senate Democrats released a competing framework in September. In December, the OCC approved five national trust bank charter applications for stablecoin issuance.

CLARITY Act Timeline

The bill hit its most significant obstacle on January 14, 2026, when the Senate Banking Committee postponed its markup session indefinitely after Coinbase and other industry participants publicly withdrew support over the stablecoin yield restrictions in the January 12 draft. Since then, the White House’s Crypto Policy Council has brokered three negotiation sessions (February 2, 10, and 19) between crypto and banking stakeholders without reaching a final agreement.Global Competitive Landscape

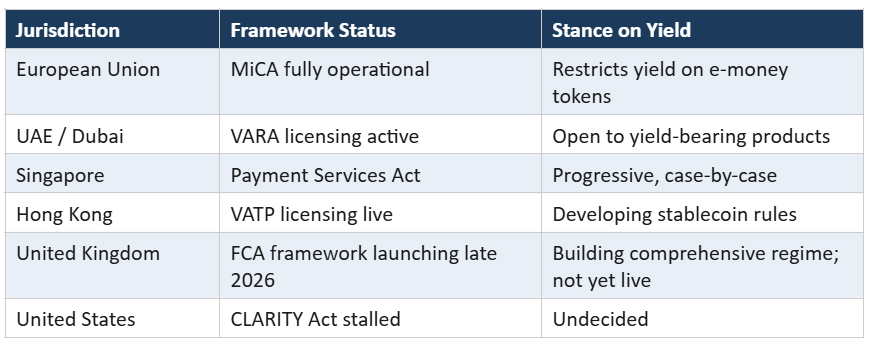

The CLARITY Act does not exist in a vacuum. The European Union’s Markets in Crypto-Assets (MiCA) framework is fully operational across all 27 member states, providing comprehensive regulatory clarity that the United States still lacks. Dubai and the UAE have positioned themselves as global crypto hubs through VARA licensing. Singapore continues to refine its Payment Services Act framework.Hong Kong has launched a licensing regime for virtual asset trading platforms. The United Kingdom is building a comprehensive FCA-regulated crypto framework expected to go live in late 2026, bringing crypto activities under the same regulatory structure as traditional financial services.

Global Regulatory Snapshot

Every month of U.S. delay is a month of competitive advantage for these jurisdictions. Several major crypto firms have already established significant operations offshore specifically because of the U.S. regulatory vacuum. At some point the migration becomes sticky enough that even strong legislation cannot fully reverse it.

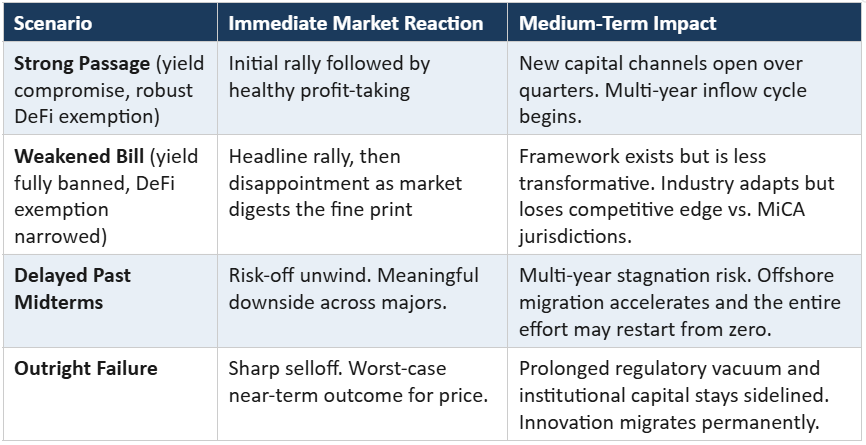

Scenario Analysis

The version of the bill that passes matters as much as whether it passes at all. A strong bill with meaningful yield provisions and a robust DeFi framework is a fundamentally different outcome from a weakened bill that bans yield entirely and narrows the DeFi exemption. The market will react to both as “CLARITY passes,” but the medium-term trajectories diverge significantly.The Implementation Gap

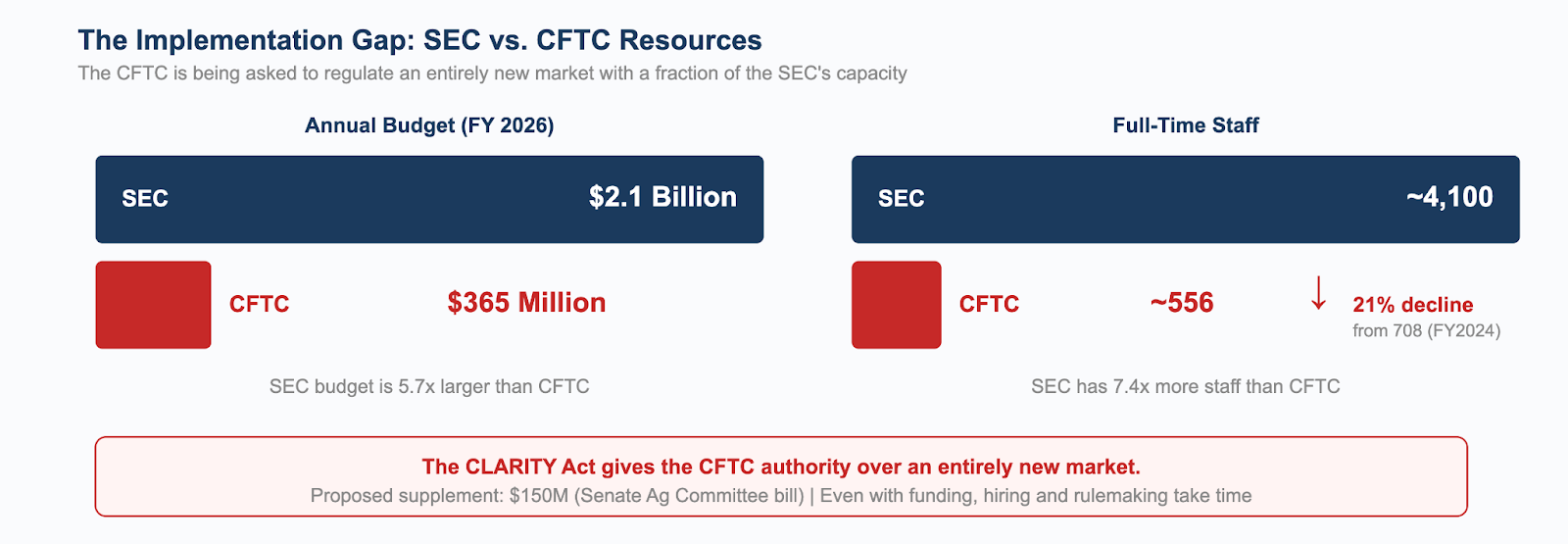

It is also important to remember that the passage does not equal immediate structural change. Even under the most optimistic legislative timeline, there is a meaningful gap between the bill being signed and the regulatory framework becoming operational. The most significant bottleneck is the CFTC itself. The CLARITY Act gives the CFTC authority over a massive new market, but the agency is dramatically smaller and less funded than the SEC.A former CFTC general counsel described the agency as “broadly understaffed” and compared the rulemaking workload to what the agency faced after Dodd-Frank, the landmark financial reform law passed after the 2008 crisis. The Senate Agriculture Committee’s bill includes a $150 million supplemental authorization and a fee-based funding mechanism. That would help, but hiring and rulemaking take time that cannot be compressed by legislation alone.

Budget and Staff data: SEC vs CFTS

The staffing numbers matter because regulation is not just about writing rules on paper. It requires people to review applications, conduct examinations, build surveillance systems, process registrations, respond to industry questions, and enforce violations.When the CLARITY Act gives the CFTC authority over an entirely new market with hundreds of exchanges, brokers, and custodians seeking registration, the agency needs the human capacity to actually process that workload. With 556 people and a fraction of the SEC’s budget, there will be a meaningful gap between the law passing and the CFTC being operationally ready to regulate what it has been given authority over.

There is also an underappreciated point about the SEC. Chairman Paul Atkins has already pulled back nearly all non-fraud enforcement actions from the prior administration, issued no-action letters to multiple digital asset issuers, and launched “Project Crypto” as an innovation sandbox.

The practical difference between a world where CLARITY passes and a world where it does not pass but Atkins stays at the SEC is smaller in the near term than the industry acknowledges. The bill’s real value is permanence: it survives a future administration change and provides a statutory foundation that cannot be reversed by the next SEC chair, which matters enormously over a multi-year horizon even if the near-term impact is more muted than the industry would have you believe.

On capital flows, the industry’s claim that “trillions in sidelined capital” will flow in is a total addressable market estimate, not a near-term flow projection. The reality is staged: first, crypto-native firms get registered and offshore operations begin repatriation; then, traditional financial institutions build products on the new framework; and only after that do institutional allocators update investment policy statements, go through committee approvals, and begin allocations.

Each phase takes time that cannot be precisely forecasted because nothing like this has happened before.

Price Action: An Honest Assessment

Bitcoin fell from $126,000 to $60,000 while the regulatory outlook was at its strongest in the asset’s history. The GENIUS Act had passed, the SEC was pulling back enforcement, and the CLARITY Act had cleared the House with bipartisan support. None of it mattered when tariffs hit, leverage cascaded, and risk assets sold off across the board. That single observation should anchor any analysis of what CLARITY means for price.The broader risk environment as of late February 2026 reinforces this point. Nvidia reported Q4 revenue of $68.1 billion, beating consensus by nearly $2 billion, with earnings per share of $1.62 versus $1.53 expected and Q1 guidance of $78 billion well above the $72.6 billion consensus. It was a beat on every metric, and the stock still fell 5.5%, erasing $260 billion in market cap within two days.

When the largest company in the world cannot rally on unambiguously good news, that is a signal about the underlying risk appetite in equity markets, and crypto does not trade in isolation from that environment.

In a neutral or positive macro environment, passage would accelerate institutional inflows and compress risk premia over a multi-year window, while in a risk-off environment it means the market falls slightly less than it otherwise would. The distinction matters because the industry consistently frames CLARITY as a catalyst, which implies it can independently move price, and the evidence from the past six months directly contradicts that framing.

The comparison most frequently invoked is the Bitcoin spot ETF approval. When ETFs were approved in January 2024, Bitcoin was trading around $46,000. Over the following 21 months, sustained institutional inflows drove the price to $126,000. That was not a sell-the-news event. It was a structural unlock that created a new channel for capital, and the flows accumulated over quarters, not days.

CLARITY would work similarly in theory: new channels (registered exchanges, compliant custody, rewritten institutional mandates) that produce sustained flows rather than a single-day pop. However, the $46K-to-$126K run happened during a broadly supportive macro environment. If CLARITY passes during a risk-off regime with equities declining and liquidity contracting, the compounding effect does not materialize in the same way.

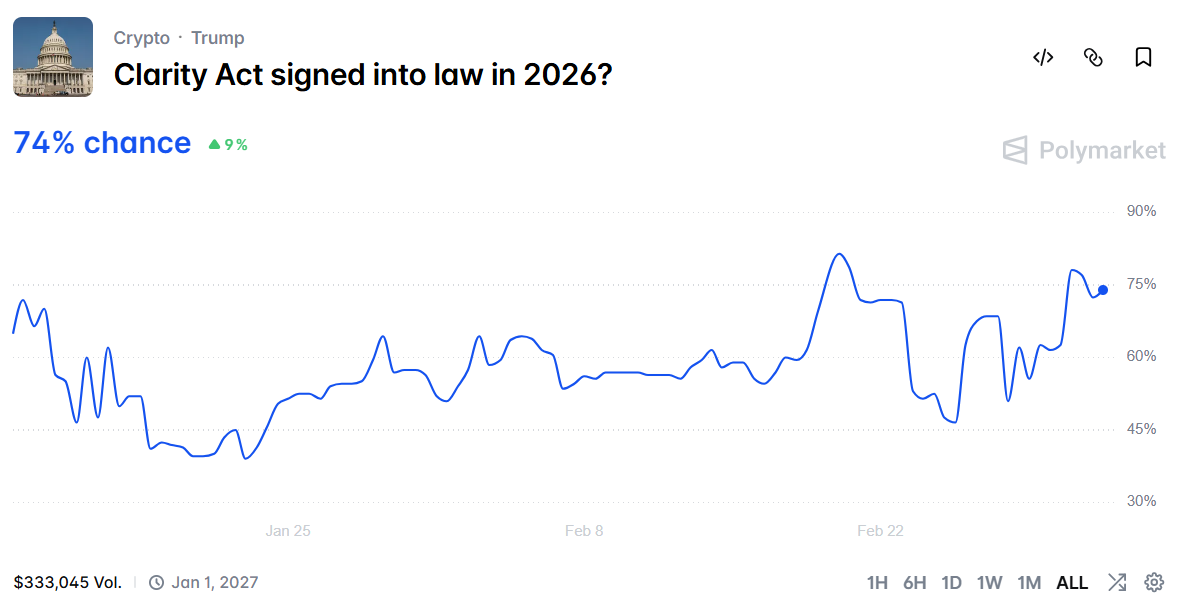

CLARITY Act passage Polymarket probability

The market has partially priced in passage. Polymarket’s 74% probability is derived from only $333,045 in total volume, which is far too thin to treat as genuine institutional conviction. Compare that to election markets on the same platform that attracted hundreds of millions in volume. Industry insiders offer higher estimates (Garlinghouse at 80 to 90%, Treasury Secretary Bessent targeting a spring signing), but these are interested parties with clear incentives to project confidence. The most independent assessments, including Citi analysts and Baker McKenzie, offer substantially more hedged views, with Citi noting a meaningful chance of delay beyond 2026.The pattern is consistent: the more confident the source, the more they benefit from passage. The more independent the source, the more hedged the assessment.

Cryptonary’s Take

The crypto industry wants you to believe the CLARITY Act is the most important thing that has ever happened. Banks want you to believe it is a threat to financial stability. The truth is somewhere in the middle and considerably more boring than either side admits.The stablecoin yield fight is the part of this story that actually matters for the long-term trajectory of the industry. Banks could compete on product quality and yield, but they are choosing to compete on political influence instead. That tells you everything about what this fight is really about. Even if idle yield gets killed in the final text, the broader framework still gives the industry a legal foundation to build on, and that foundation is what everything else gets built on.

Here is what we know for certain. The bill passed the House with strong bipartisan support and is stalled in the Senate over stablecoin yield. Three rounds of White House-brokered negotiations have produced no deal. The real deadline is the November 2026 midterms, and the CFTC is severely underfunded relative to what the bill asks it to do.

Here is what we do not know. We do not know what the final bill text will look like, and the gap between a strong bill and a weak bill is enormous. We do not know how fast institutional capital would actually flow in even in the best-case scenario. We do not know what the macro environment will look like when and if the bill passes. And we do not know whether a future administration would respect the framework or attempt to reverse it.

Over the next 90 days, there are five things worth paying attention to. Whether the Senate Banking Committee reschedules its markup is the single clearest signal of whether the bill is moving or stalling, because until a date is set, the bill is effectively frozen regardless of what insiders say publicly.

Any publicly circulated draft language distinguishing between idle yield and activity-based rewards would indicate the compromise is taking shape, because without agreed-upon language, no vote happens. Shifts in tone from the banking lobby matter too: if the Bank Policy Institute or ABA moves from demanding a complete yield ban to negotiating specific thresholds or exemptions, the deal is closer than headlines suggest.

Congressional attention to CFTC funding and staffing capacity will indicate whether lawmakers are serious about implementation or simply passing a bill to claim credit before midterms. And finally, none of the above matters if the macro environment deteriorates meaningfully, because the S&P 500, Fed policy signals, and global liquidity conditions will drive crypto prices more than any legislative development.

The infrastructure underneath crypto has never been stronger. Regulated ETFs, federal stablecoin law, institutional-grade custody, real lending markets, real derivatives markets. These are operational realities.

What has been missing is the legal framework that ties it all together and survives a change in administration. The CLARITY Act is that framework. Whether it arrives in a strong form, a weakened form, or not at all remains the open question.

We will react to it in real-time, and subscribers get early access to our models and execution plans: the same disciplined process that has guided our calls through major macro and regulatory shifts.

If you want to stay ahead of the curve instead of reacting to it, you know where to be.

Peace!

Cryptonary, OUT!

Continue reading by joining Cryptonary Pro

$1,548 $1,197/year

Get everything you need to actively manage your portfolio and stay ahead. Ideal for investors seeking regular guidance and access to tools that help make informed decisions.

For your security, all orders are processed on a secured server.

As a Cryptonary Pro subscriber, you also get:

3X Value Guarantee - If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund. Terms

24/7 access to experts with 50+ years’ experience

All of our top token picks for 2025

On hand technical analysis on any token of your choice

Weekly livestreams & ask us anything with the team

Daily insights on Macro, Mechanics, and On-chain

Curated list of top upcoming airdrops (free money)

3X Value Guarantee

If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut through the noise and consistently find winning assets.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut

through the noise and consistently find winning assets.

Frequently Asked Questions

Can I trust Cryptonary's calls?

Yes. We've consistently identified winners across multiple cycles. Bitcoin under $1,000, Ethereum under $70, Solana under $10, WIF from $0.003 to $5, PopCat from $0.004 to $2, SPX blasting past $1.70, and our latest pick has already 200X'd since June 2025. Everything is timestamped and public record.

Do I need to be an experienced trader or investor to benefit?

No. When we founded Cryptonary in 2017 the market was new to everyone. We intentionally created content that was easy to understand and actionable. That foundational principle is the crux of Cryptonary. Taking complex ideas and opportunities and presenting them in a way a 10 year old could understand.

What makes Cryptonary different from free crypto content on YouTube or Twitter?

Signal vs noise. We filter out 99.9% of garbage projects, provide data backed analysis, and have a proven track record of finding winners. Not to mention since Cryptonary's inception in 2017 we have never taken investment, sponsorship or partnership. Compare this to pretty much everyone else, no track record, and a long list of partnerships that cloud judgements.

Why is there no trial or refund policy?

We share highly sensitive, time-critical research. Once it's out, it can't be "returned." That's why membership is annual only. Crypto success takes time and commitment. If someone is not willing to invest 12 months into their future, there is no place for them at Cryptonary.

Do I get direct access to the Cryptonary team?

Yes. You will have 24/7 to the team that bought you BTC at $1,000, ETH at $70, and SOL at $10. Through our community chats, live Q&As, and member only channels, you can ask questions and interact directly with the team. Our team has over 50 years of combined experience which you can tap into every single day.

How often is content updated?

Daily. We provide real-time updates, weekly reports, emergency alerts, and live Q&As when the markets move fast. In crypto, the market moves fast, in Cryptonary, we move faster.

How does the 3X Value Guarantee work?

We stand behind the value of our research. If the documented upside from our published research during your 12-month membership does not exceed three times (3X) the annual subscription cost, you can request a full refund. Historical context: In every completed market cycle since 2017, cumulative documented upside has exceeded 10X this threshold.

TermsRecommended from Cryptonary