Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 44s

“The Everything Exchange” and Its Unprecedented Equity Bet

Another free money drop! We covered how to qualify for this airdrop in our previous report. This piece focuses on post-TGE navigation and evaluates this token as a potential investment. While the timeline is flooded with FUD and misinformation, the purpose of this report is to cut through the noise and clarify what is actually true, what the real risks are, and what the opportunity looks like. Let’s dive in…

In this report:

- What happened at the $BP TGE, and why price fell short of expectations (so far)

- What Backpack actually is, and why the product matters

- How the equity exchange program works in practice

- The math on when staking beats selling

- Where Backpack sits relative to Coinbase, Kraken, Robinhood, and peers

- The key risks, opportunity costs, and decision framework for holders

Disclaimer: This is not financial or investment advice. You are responsible for any capital-related decisions you make, and only you are accountable for the results.

What Happened

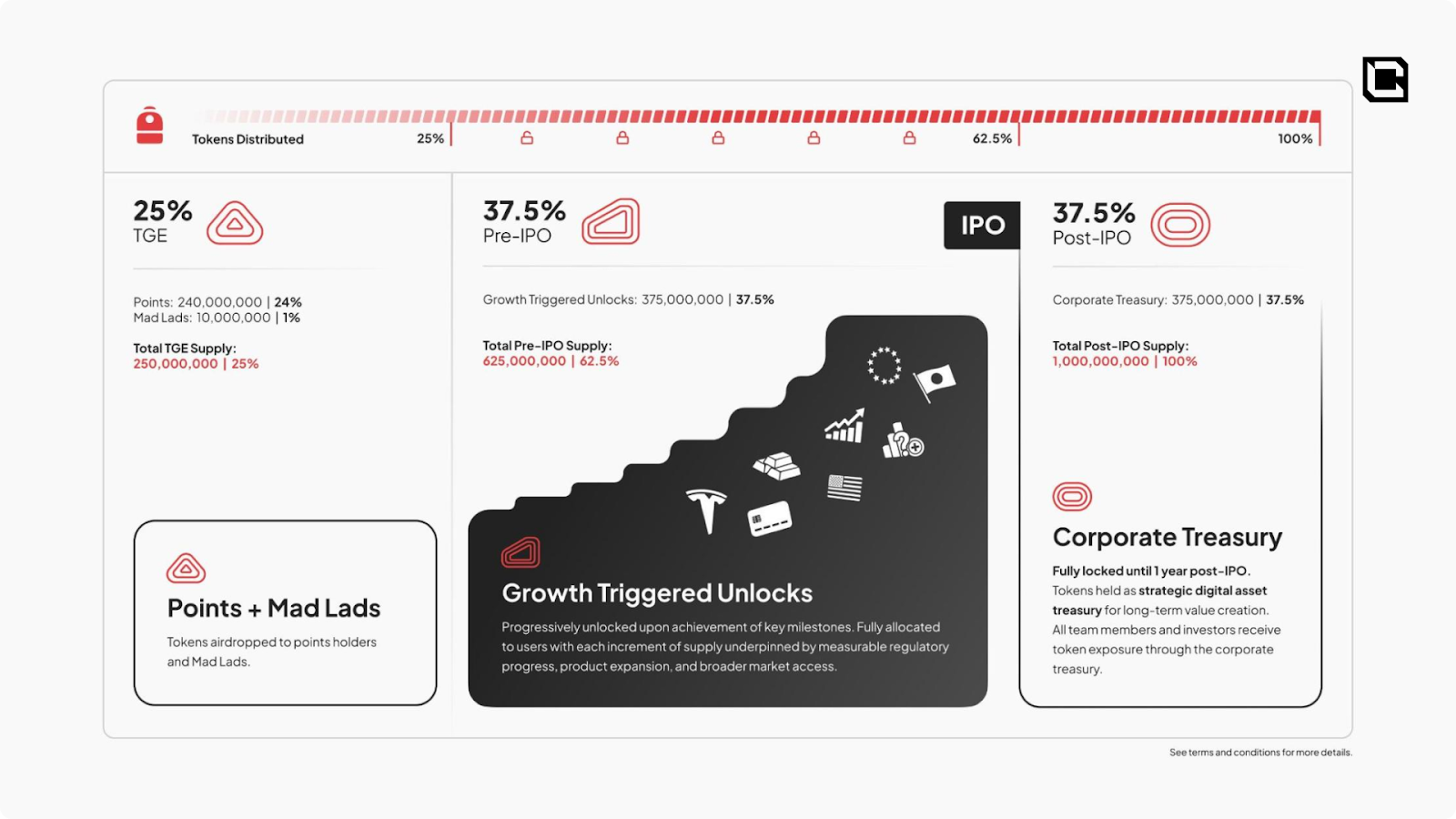

On March 23, 2026, Backpack Exchange launched $BP on Solana. At TGE, 250 million tokens, or 25% of the 1 billion total supply, were distributed entirely to the community: 240 million to “Points” program participants and 10 million to Mad Lads NFT holders. Zero tokens were allocated to founders, team members, or investors at launch.

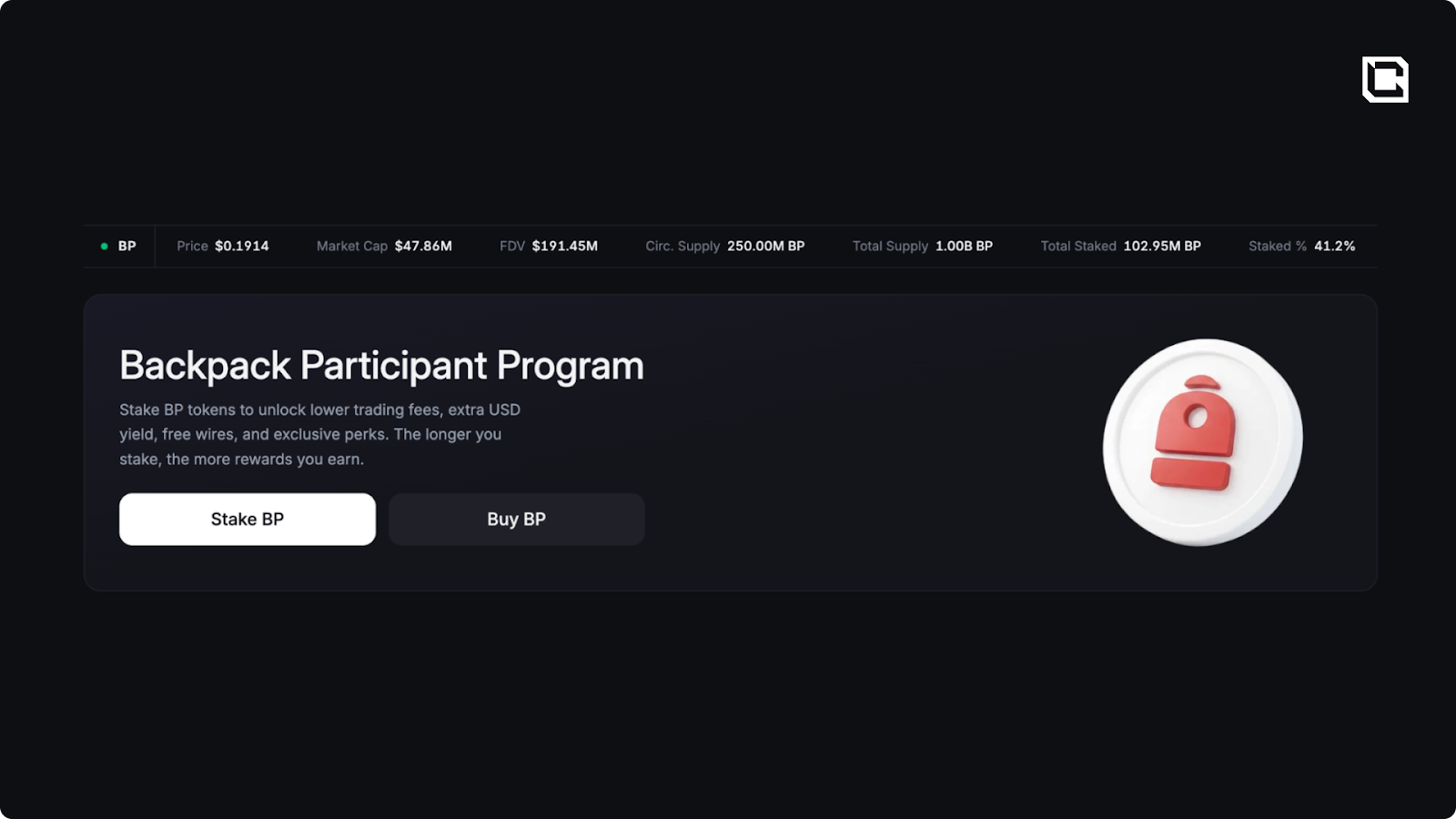

From an execution standpoint, the launch was technically clean. The token reached a high of roughly $0.26 and a low around $0.175, and has since consolidated in the $0.19 to $0.20 range. As of writing, $BP is trading at $0.198 on Backpack Exchange, implying a circulating market cap of $49 million and an FDV of $198 million.

$BP launched into one of the worst sentiment environments of the cycle. The Fear & Greed Index sat at 11, or Extreme Fear. The US-Iran conflict was in its fourth week. Kraken had frozen its own IPO. Other recent perp and exchange-adjacent TGEs, including $DIME and $LIT, also sold off sharply after launch. Releasing a token into that backdrop took conviction.

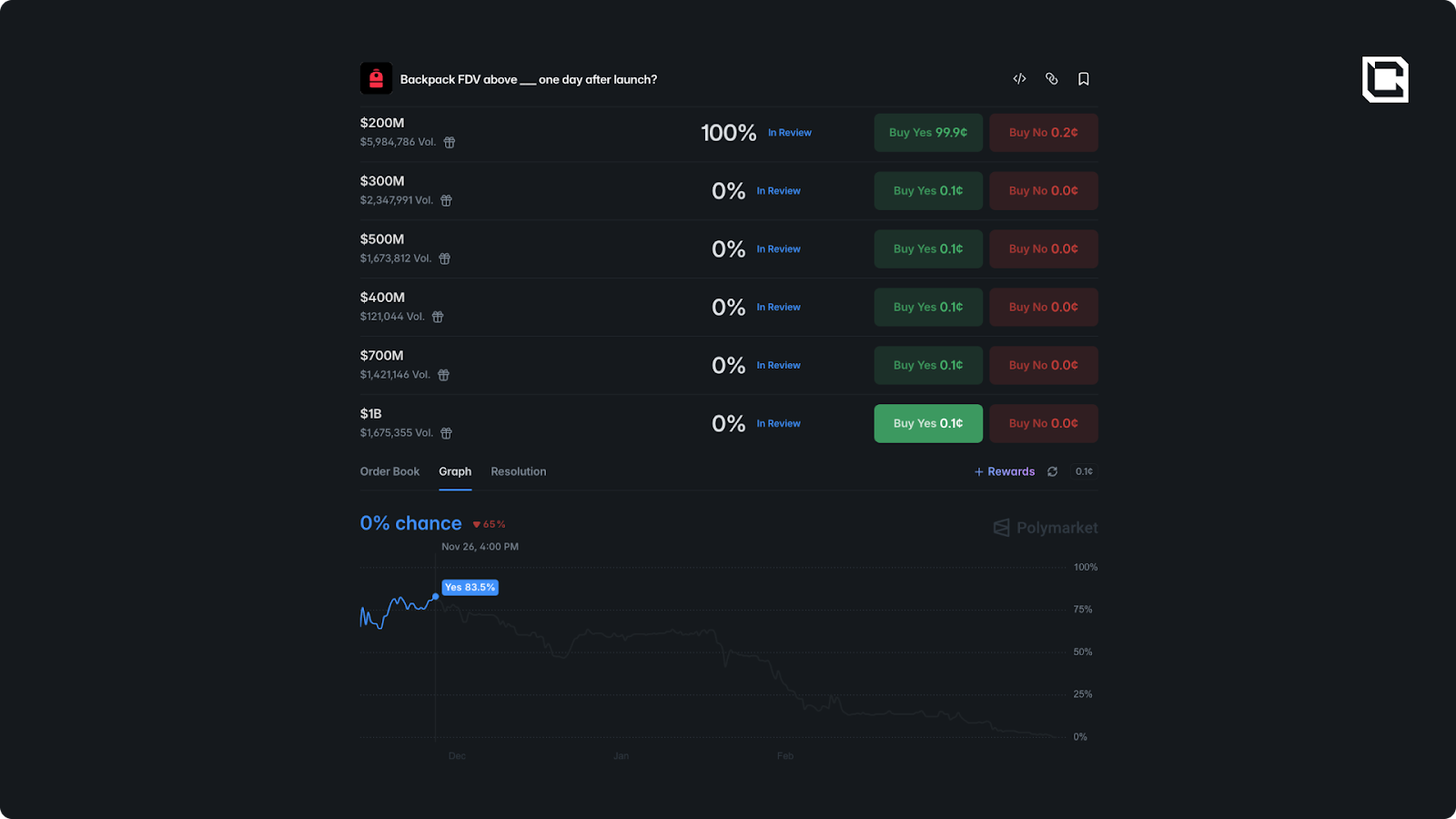

Back in November 2025, when market sentiment was significantly stronger, Polymarket had priced an 83.5% chance of $BP reaching an FDV above $1 billion. The gap between those expectations and current reality is the main source of community frustration, not any obvious fundamental issue with the project.

What Backpack Actually Is

Let's start with the team behind Backpack. Armani Ferrante built Anchor, the framework that powers much of Solana’s onchain ecosystem. He also built the Backpack wallet, the first xNFT wallet, and launched Mad Lads (Solana’s leading NFT collection). Ferrante is a UC Berkeley computer science graduate and a former Apple software engineer, but the more important point is that he has a rare track record of shipping infrastructure that actually gets used.

Co-founder Tristan Yver previously served as general counsel at FTX and later testified against Sam Bankman-Fried. Backpack has also appointed Mark Wetjen, former CFTC Commissioner and Acting Chairman, as President of Backpack US. Taken together, the team gives Backpack more credibility than a typical exchange startup.

The Product Suite

Backpack is vertically integrated. Its wallet, exchange, and upcoming securities platform are all being built into a single unified margin system. It is one of the clearest attempts in crypto to bridge CeFi and DeFi inside a single product stack.

Everything runs through one cross-margined account:

- spot trading

- perpetual futures across 73 pairs with up to 50x leverage

- borrow and lending

- prediction markets

- multi-chain wallet with zero-fee swaps across more than 15 networks. I

Backpack also supports fiat on and off ramps through USD bank transfers, while allowing direct crypto deposits across multiple ecosystems, including native BTC and HyperEVM. That gives users a more direct bridge into the trading stack rather than forcing everything through external exchanges or payment apps.

The value proposition extends beyond the token itself. In addition to the main airdrop, active users have also been able to earn through lending and staking yield, referrals, and other ecosystem rewards.

In total Backpack:

- Processed $434b in volume

- $282m in capital lent

- $55m in capital borrowed

You’ll be able to transfer stocks from your pre-existing brokerage account into Backpack, trade, and use them as collateral for the rest of the margin system.” Backpack’s partnership with Superstate covers more than just on-chain IPO allocations. It also underpins the broader push into tokenized public equities, with IPO access serving as one part of a larger on-chain securities strategy.

Revolut is not a direct comp, but it is a useful vision comp. Revolut built a roughly $75 billion business by starting with banking and payments, then layering in crypto, stocks, and broader financial services.

Backpack is attempting the inverse: starting with a crypto-native exchange and wallet, then expanding into banking rails and tokenized securities. The starting point, customer base, and acquisition strategy are very different, which is why Revolut does not belong in the main comparison table. But the end-state ambition is similar enough that it helps frame the size of the opportunity if Backpack executes.

Regulatory Moat & Key Metrics

Backpack holds a VARA VASP license in Dubai, MiFID II authorization via CySEC in Europe, JVCEA Type 2 registration in Japan, and FinCEN registration in the United States. It is one of only two platforms, alongside Kraken, currently offering regulated perpetual futures in Europe. A U.S. launch is planned for next month.

Tokenomics

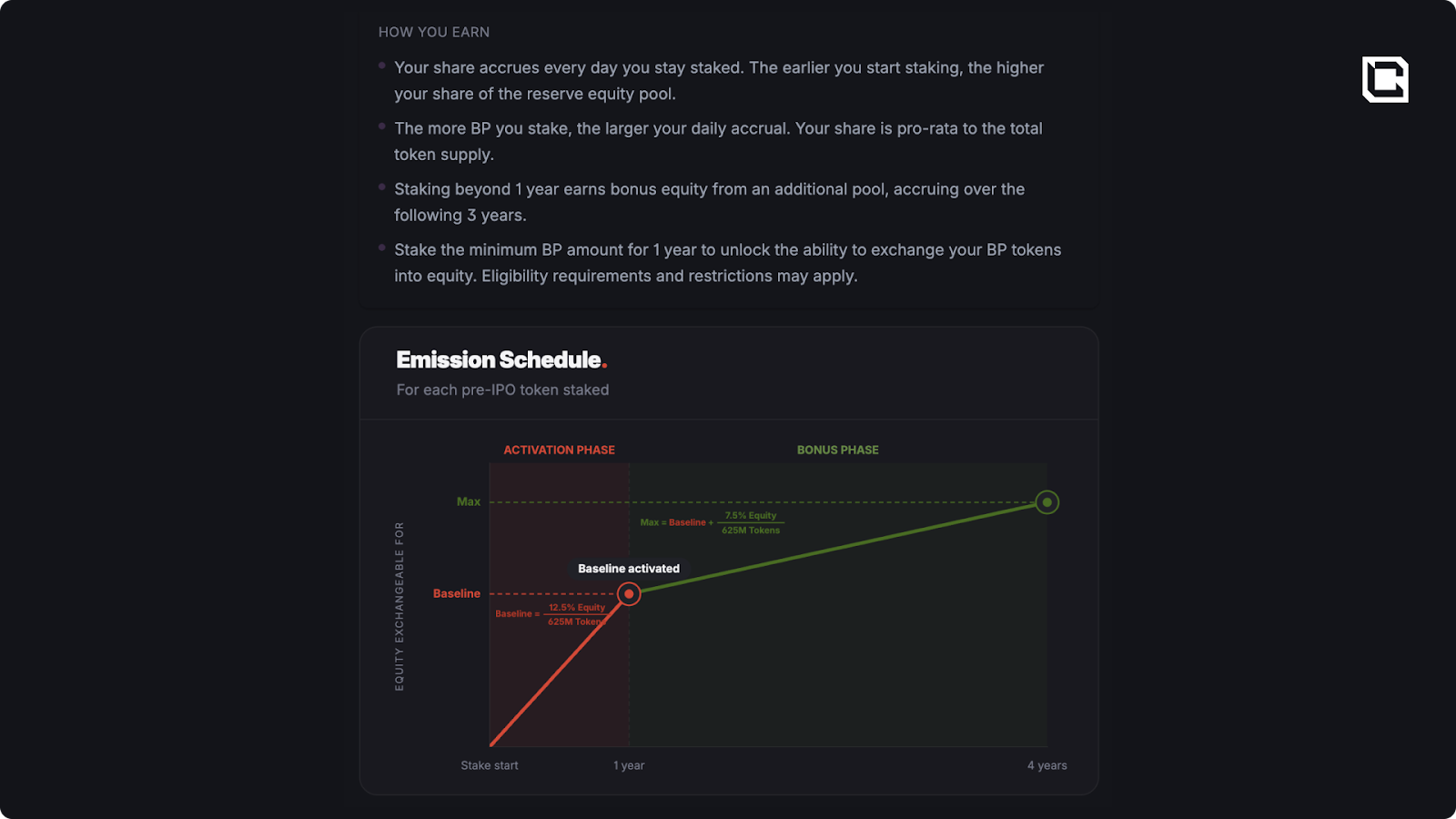

This is what makes $BP different from almost every other exchange token in crypto. Backpack is offering stakers the ability to exchange tokens for actual company equity. There is no clean precedent for this structure.Base Activation Phase: Stake for a minimum of one year. Equity entitlement is calculated as:

(your staked tokens / 1 billion total supply) × 20% of company equity as of February 23, 2026

The 625 million pre-IPO tokens, consisting of the TGE allocation and growth unlocks, form the basis for the equity exchange calculation. The remaining 375 million sits in post-IPO corporate treasury, which means the team’s economic upside is deferred until after the community has already had a meaningful head start.

This amount activates as a lump sum after the full one-year period. Importantly, the program math is based on the 625 million pre-IPO token allocation rather than the full eventual token supply.

Bonus Phase: Tokens staked beyond the first year continue accruing additional equity from a separate 7.5% pool, distributed over three years across the 625 million pre-IPO token allocation. If the IPO occurs before the full bonus period ends, remaining bonus emissions stop and the undistributed portion is forfeited back to the company.

The key condition is that tokens must remain staked until the Backpack Exit Event, whether that is an IPO or an equivalent liquidity event. That requirement may feel harsh to some users, but the logic is straightforward. If someone could stake for one year, sell their tokens, and still retain IPO upside, the structure would be economically broken. Participants would keep the equity upside without continuing to bear the same long-duration risk as everyone else.

Unstaking resets the clock on those tokens. There is also a seven-day cooldown period on unstaking, though this is currently instant during the launch period. Participants must also remain Monthly Active Users, defined as at least one platform action per month. The equity itself is held through SPVs, which is a standard structure for distributing equity at scale across large groups of participants.

Disclaimer: This is our interpretation of publicly available documentation. We are not legal or financial advisors. Review the official Backpack Participant Program T&Cs and consult your own counsel.

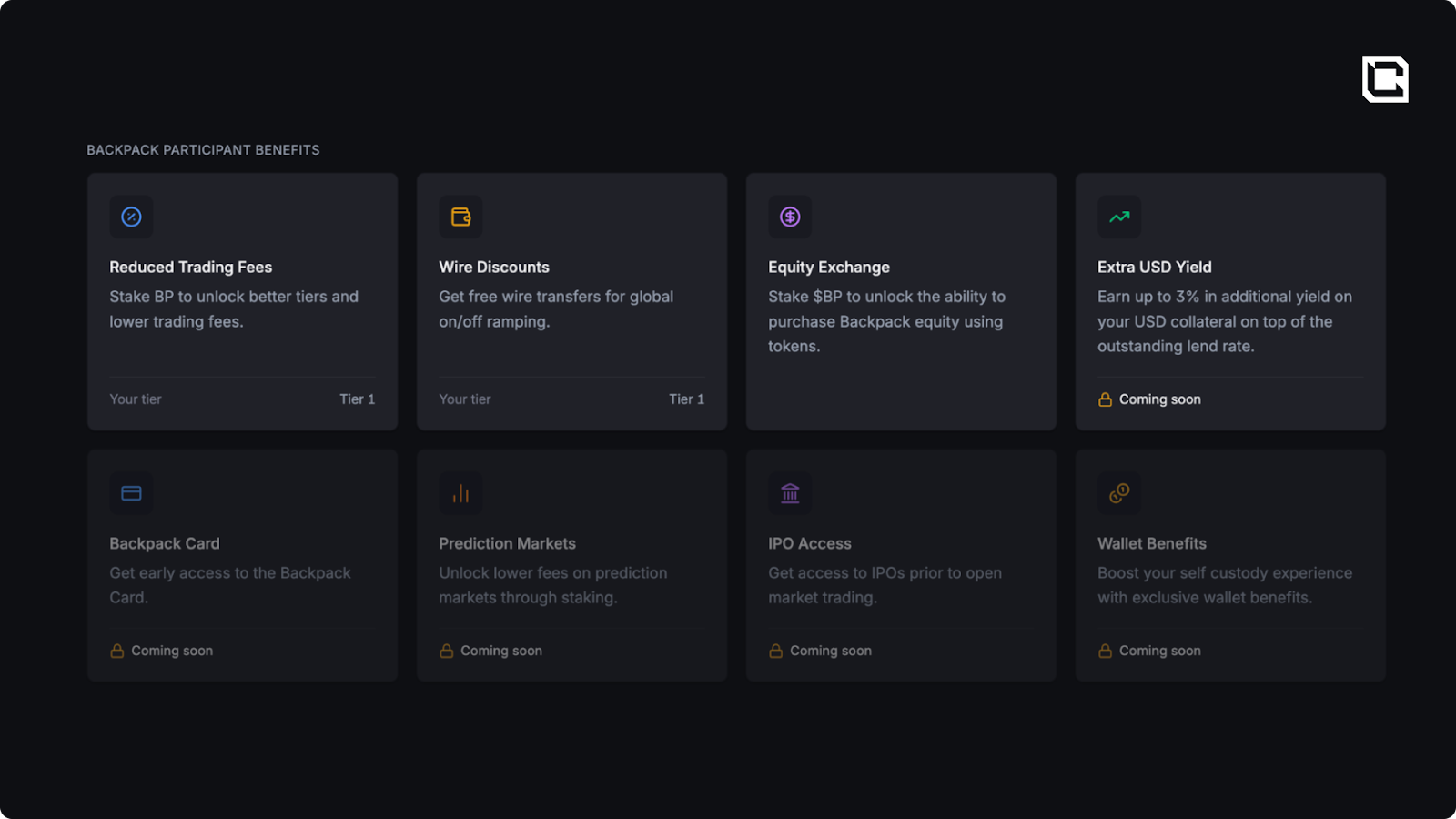

Token Utility Beyond Equity

Staking unlocks immediate value even before the equity clock starts. Benefits include tiered maker and taker fee discounts on spot and perpetuals, reduced or waived fiat on and off-ramp fees, boosted USD collateral yields of up to 3%, and priority access to new product launches, including on-chain IPO allocations.

The equity conversion creates an unusual pricing structure for $BP. Unlike most tokens, where price is driven mainly by speculation and narrative cycles, $BP is at least partly anchored to expectations around a future IPO.

On the upside, that may place a soft ceiling on the token. If $BP rallies to a point where selling in the market offers a better risk-adjusted outcome than staking for future equity, rational holders may choose to sell rather than lock up. That does not mean the token cannot rise meaningfully, but it does suggest upside may be more constrained than a typical reflexive exchange token. Do not expect meme-coin style price action.

On the downside, the equity conversion can also create a form of valuation support. If the token falls far enough below what long-term holders believe the future equity could be worth, buyers with capital and conviction may step in and accumulate. That does not make the token risk-free, but it does create a level below which the equity-linked value proposition becomes harder to ignore.

The result is a token that may behave less like a pure speculative asset and more like a discounted claim on future company value. A meaningful portion of the ultimate price discovery may happen at IPO, but the path there will still depend on execution. U.S. launch, real securities rollout, sustained volume growth, and eventual clarity around timing all have the potential to re-rate the token well before any listing event becomes real

The Math: Sell Now vs. Stake for IPO

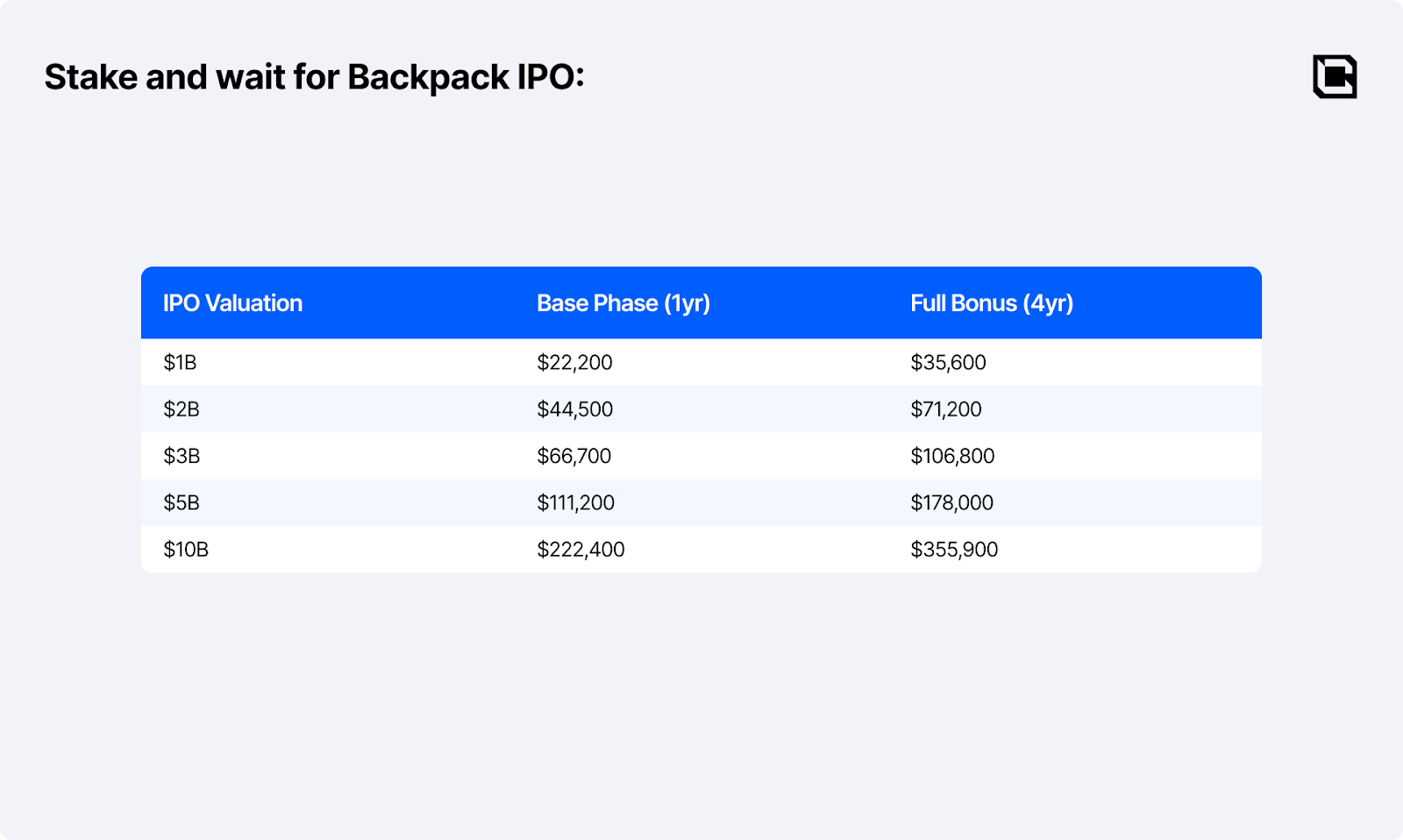

This is the key economic question. Using a 111,204 $BP allocation (one of our team member's allocation) as an example:- Sell at current price ($0.20): $22,200

- But...

The honest truth is that a $1 billion IPO barely justifies the lockup. You would wait one to four years for an outcome that is roughly in line with selling today. The staking bet only starts to look compelling if you believe Backpack can IPO at $5 billion or more, where the returns begin to meaningfully outperform an immediate sale. A great deal needs to go right for that to happen: a successful U.S. launch, real securities rollout, sustained growth in trading activity, and a favorable IPO window. But if Backpack executes through the next bull cycle, a $5 billion to $10 billion valuation is not outside the range of comparable exchanges.

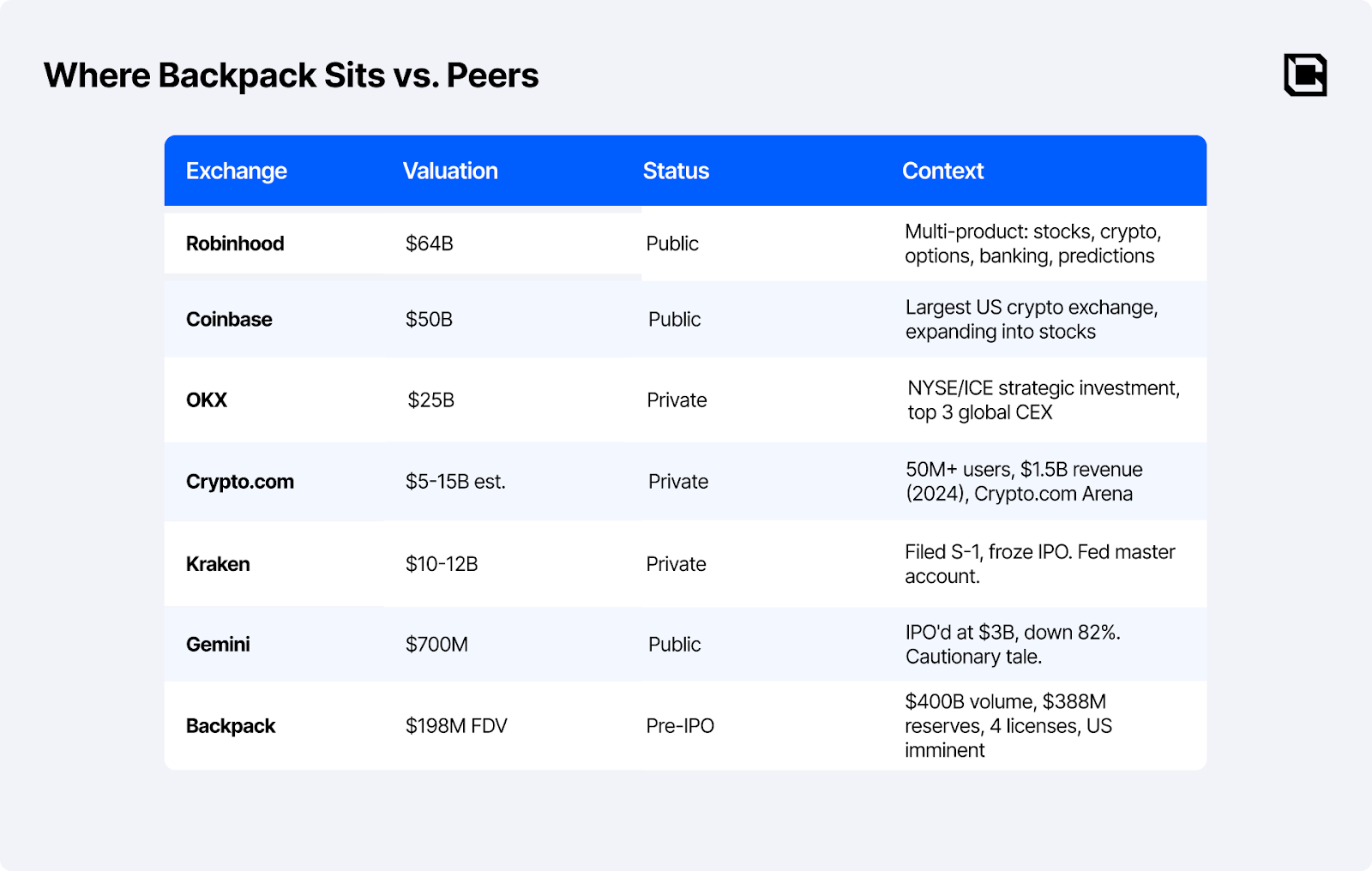

The gap between Backpack’s current $198 million FDV and even Kraken at $10 billion is more than 50x. That is what makes the story interesting. But Gemini’s drop from $3 billion to roughly $700 million is a reminder that exchange valuations can compress just as violently as they expand. The gap shows both the size of the opportunity and how early Backpack still is. Probably both.

The Opportunity Cost Question

This is the strongest bear argument. What else could you do with $22K over 3-4 years?- Stablecoin yield (5-8% APY): $3,000-6,700 in cumulative interest, with lower principal volatility and much higher liquidity.

- BTC accumulation at current levels: If BTC returns to $126K ATH, roughly 2x. A move to $200K+ in the next cycle is 3x.

- Airdrop farming: A strategy Cryptonary members are well-positioned for if they follow our guides. Deploying capital across multiple farms can generate multiples through token drops.

- Other early-stage token plays: The capital could rotate across shorter-duration opportunities with faster feedback loops.

The Bull Case

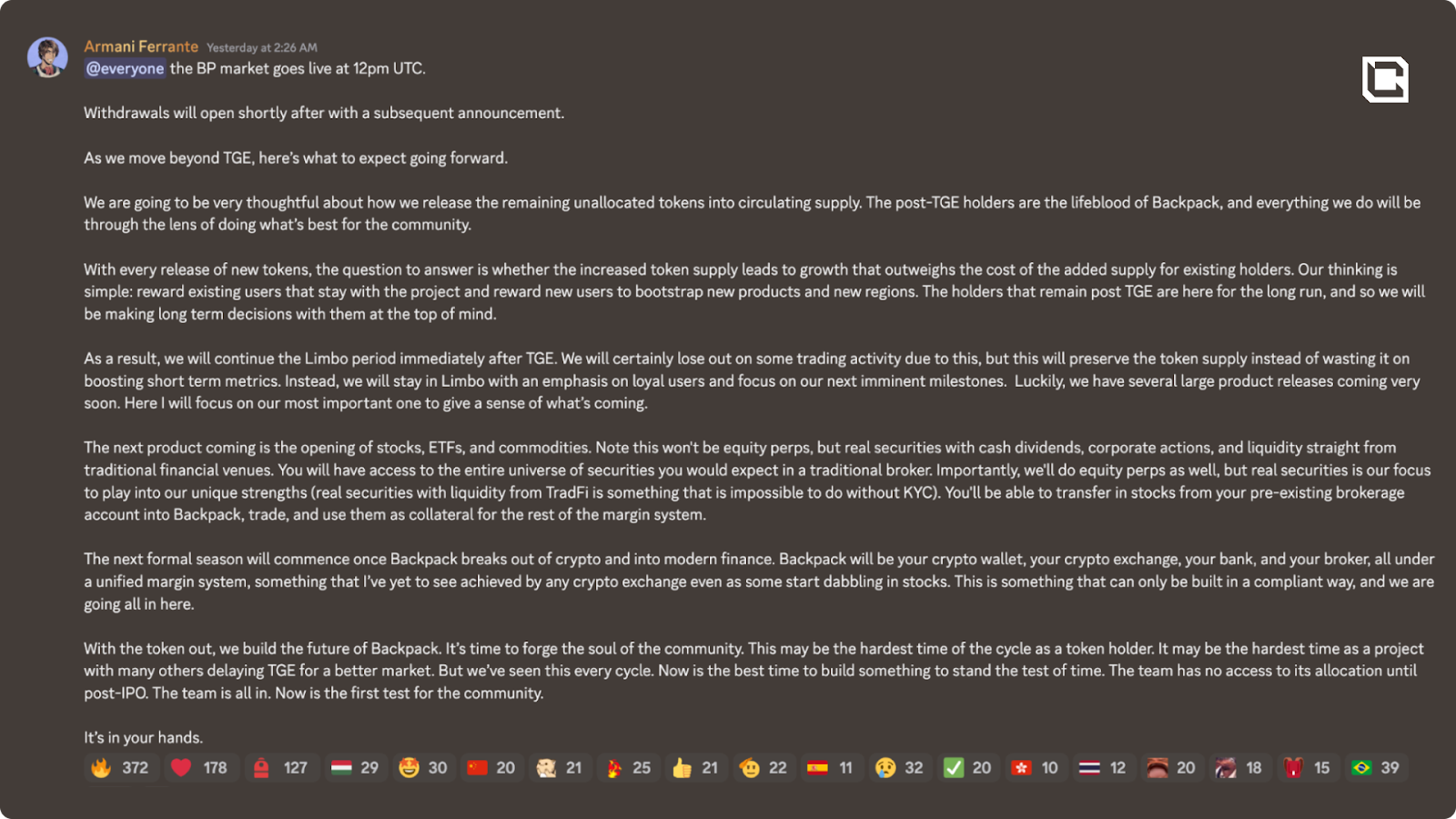

Team alignment is unusually strong. 37.5% of supply sits in corporate treasury and remains locked until one year after IPO, with no separate team allocation. As Armani put it, “The team has no access to its allocation until post-IPO. The team is all in.” In other words, the team’s economic upside is tied to the same outcome long-term holders are betting on: a successful IPO.That alignment appears to be reflected in user behavior. 41.2% of circulating supply was staked on day one, meaning nearly half of the available float was locked by holders choosing the equity path rather than immediate liquidity. That is a strong conviction signal and it meaningfully reduces near-term sell pressure.

The product roadmap also matters. Real securities via Superstate are expected next, including stocks, ETFs, and commodities with cash dividends that can be traded inside the unified margin system and used as collateral. If Backpack delivers that, it becomes something meaningfully different from a standard crypto exchange.

U.S. expansion is the other major catalyst. It is planned for next month, with a former CFTC Commissioner leading the effort. That opens the door to the single largest pool of crypto users and capital that Backpack does not currently serve. The exact magnitude of that opportunity is still uncertain, but the directional logic is straightforward: if Backpack can pair a U.S. launch with real securities and its unified margin system, the upside from here becomes much easier to underwrite.

The Bear Case

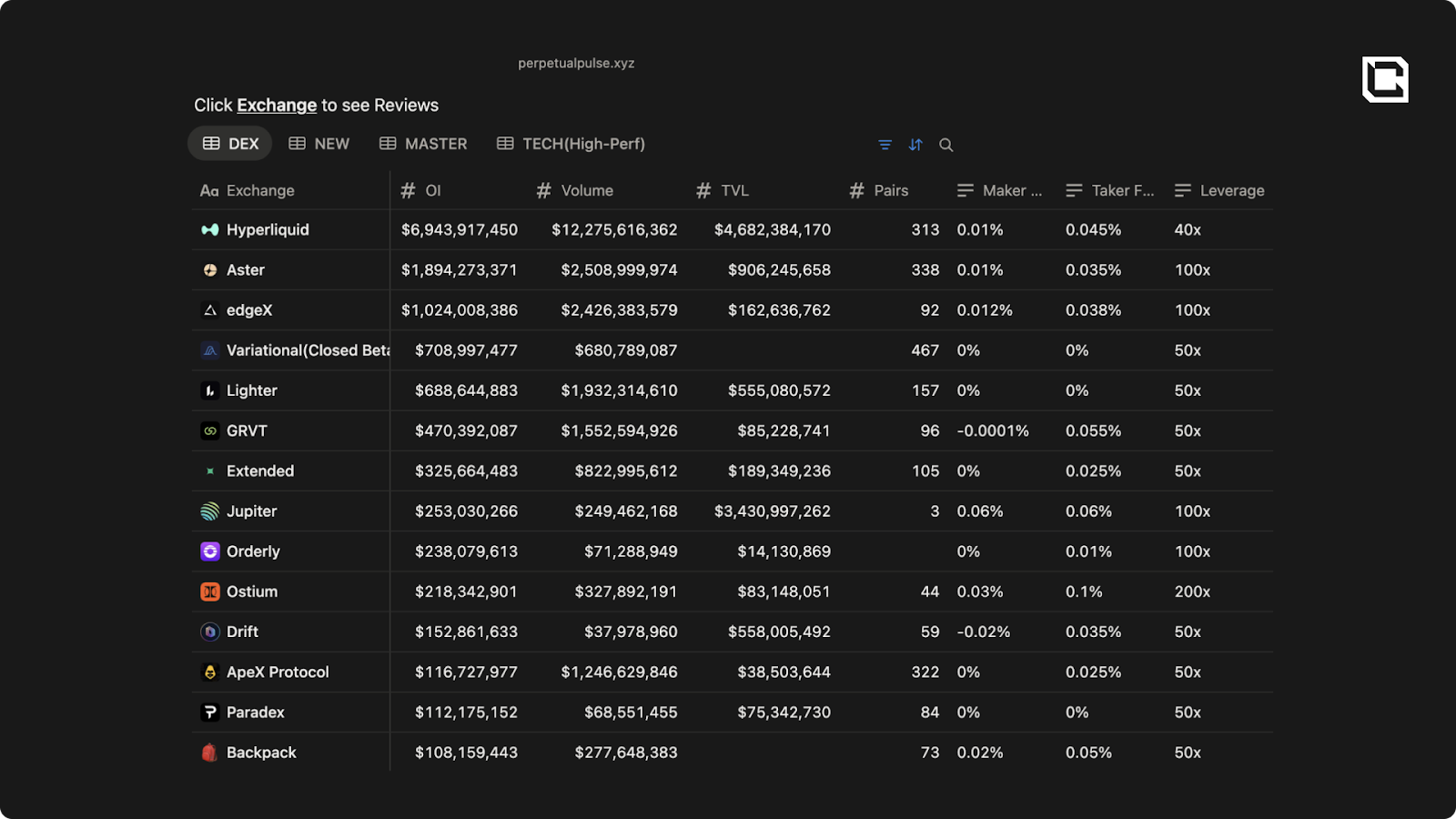

The launch was disappointing relative to expectations. $BP is trading around $0.20, far below the November market expectation of a $1 billion-plus FDV. The macro backdrop clearly hurt sentiment, but that does not change the outcome for holders who expected a much stronger launch.Backpack’s core trading metrics also remain far behind the category leader. Perpetual open interest sits around $108 million, versus roughly $6.9 billion on Hyperliquid. Backpack is not just a perp venue, but those numbers still need to scale meaningfully if the broader “Everything Exchange” thesis is going to hold.

The Mad Lads allocation also felt thin. Just 1% of supply was spread across roughly 6,600 holders, despite Mad Lads being one of Backpack’s most loyal communities and a group that had already received meaningful value from earlier ecosystem distributions such as Wormhole. Relative to the NFT’s historical floor prices, the $BP allocation felt light, even if the collection has declined significantly from its peak near 200 SOL.

The equity path also comes with real time risk. Holders must stake for at least one year and then remain staked until an IPO or equivalent exit event. There is no guaranteed timeline. Kraken has already frozen its own IPO, and Gemini’s public-market outcome is a reminder that listing does not automatically create value. If Backpack takes several years to reach an exit, and that exit comes at only $1 billion, the economics barely outperform selling today.

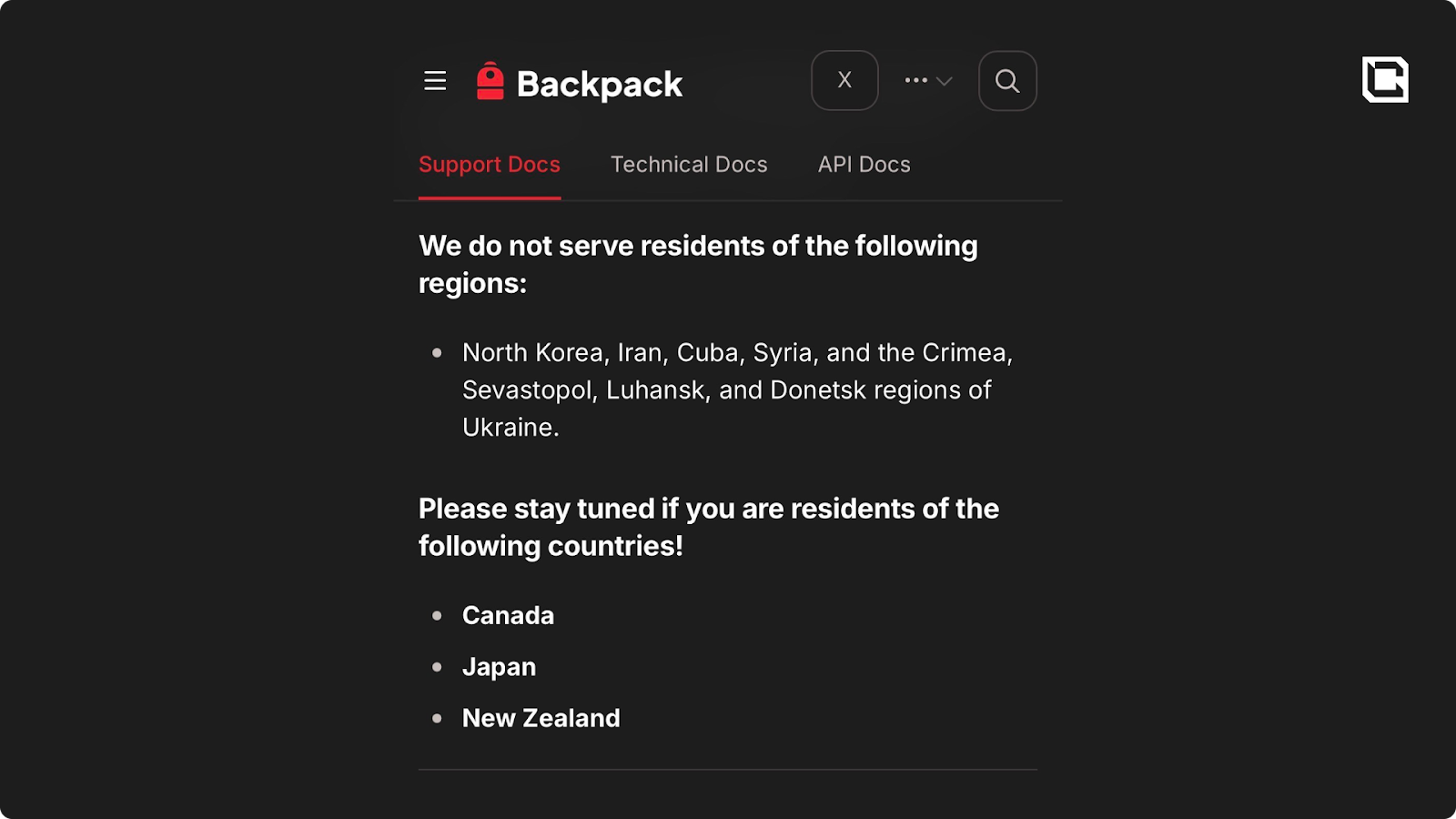

Finally, access is not universal. The equity exchange requires accredited investor verification in the United States, or an equivalent standard in other jurisdictions, and some regions are not currently served at all. Backpack’s own support docs list countries such as Canada, Japan, and New Zealand as markets that are not yet supported. That means the most attractive part of the token’s long-term value proposition is not equally available to every holder.

What Holders Need to Be Right About

The staking thesis ultimately reduces to one bet: Backpack needs to execute on real securities, launch successfully in the U.S., grow trading volume materially, maintain regulatory progress, and reach an IPO at $5 billion or more within a reasonable timeframe.That is a demanding list, and every part of it matters. The legal terms give Backpack significant discretion, the shares are non-voting, there is no guaranteed timeline, and the equity sits inside an SPV that cannot be exited until the company chooses to distribute. Those are real structural risks, even if you trust the team.

KPIs We're Watching (6-12 Months)

- US launch: Does it actually happen next month, and what does early traction look like?

- Real securities launch: Does Superstate-powered stock trading go live, and does it attract meaningful activity?

- Volume growth: Perpetual open interest needs to scale from $108 million toward $500 million-plus as an initial milestone, with materially higher levels needed over time to justify exchange-tier valuations.

- Staked supply: Does the initial staked supply of 41.2% hold, or does it begin to bleed as patience wears thin?

The Decision Framework

- Sell: Take guaranteed value. This is the right choice if you need capital, do not believe in a $5 billion-plus IPO, or can deploy elsewhere with higher conviction.

- Stake: Commit to the equity path. This makes sense if you believe in a $5 billion-plus IPO, are comfortable with a multi-year lockup, meet the KYC requirements, and are willing to remain monthly active.

- Hold liquid: Preserve optionality. This allows you to sell into strength, stake later if conviction improves, or continue using the token for fee discounts and platform benefits. You give up equity accrual, but retain flexibility.

Our suggested framework for airdrop recipients is 30/30/30/10:

- sell 30% to lock in value

- stake 30% for the equity conversion

- keep 30% liquid for optionality, and leave 10% as a buffer

Cryptonary's Take

What Backpack is attempting is genuinely unprecedented. Most projects launch tokens and hope the market assigns value through speculation. Backpack is making a much more explicit proposition: the long-term value lies in equity in a company building toward an IPO. The team cannot access its allocation until after that event. They cannot simply extract value and move on. They have to execute. That alignment structure is rare anywhere in business, let alone crypto.The product is real. We have used it extensively first-hand. The unified margin account, lending rates, perp execution, and zero-fee wallet are all competitive. The regulatory portfolio is unusually strong for a company at this stage. Real securities are coming and the U.S. launch is imminent. Armani Ferrante built the framework much of Solana runs on and has a rare track record of shipping infrastructure that actually matters. That gives Backpack more credibility than most early exchange projects.

The bear case still deserves respect. The token launched into a brutal market. Perp volumes remain a fraction of the leader’s. The equity path requires a multi-year lockup with no guaranteed IPO timeline. Opportunity cost is real.

But every launch this month has struggled. $DIME and $LIT are both down significantly as well. HYPE is the only token performing in this environment, and comparing a new launch to the market leader during extreme fear is not a fair benchmark.

A personal note: we usually dump airdrop tokens immediately and move on to the next farm. That has been the playbook, and it has worked well. Backpack is the first project in a long time that has made us genuinely pause and reconsider. That does not mean we are blindly bullish. It means the equity conversion structure is different enough from anything we have seen before that it deserves serious evaluation rather than a reflexive sell.

The honest bottom line is simple. If you believe crypto exchanges will grow and Backpack can reach a $5 billion-plus valuation over the next three to four years, the current price offers potential equity-linked upside at a tiny fraction of peer valuations. If you do not have that level of conviction, selling and rotating elsewhere is completely reasonable. And if you are genuinely uncertain, uncertainty is best met with diversification, not forced conviction. That is exactly what the 30/30/30/10 framework is designed for.

Cryptonary, OUT!

Continue reading by joining Cryptonary Pro

$1,548 $1,197/year

Get everything you need to actively manage your portfolio and stay ahead. Ideal for investors seeking regular guidance and access to tools that help make informed decisions.

For your security, all orders are processed on a secured server.

As a Cryptonary Pro subscriber, you also get:

3X Value Guarantee - If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund. Terms

24/7 access to experts with 50+ years’ experience

All of our top token picks for 2025

On hand technical analysis on any token of your choice

Weekly livestreams & ask us anything with the team

Daily insights on Macro, Mechanics, and On-chain

Curated list of top upcoming airdrops (free money)

3X Value Guarantee

If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut through the noise and consistently find winning assets.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut

through the noise and consistently find winning assets.

Frequently Asked Questions

Can I trust Cryptonary's calls?

Yes. We've consistently identified winners across multiple cycles. Bitcoin under $1,000, Ethereum under $70, Solana under $10, WIF from $0.003 to $5, PopCat from $0.004 to $2, SPX blasting past $1.70, and our latest pick has already 200X'd since June 2025. Everything is timestamped and public record.

Do I need to be an experienced trader or investor to benefit?

No. When we founded Cryptonary in 2017 the market was new to everyone. We intentionally created content that was easy to understand and actionable. That foundational principle is the crux of Cryptonary. Taking complex ideas and opportunities and presenting them in a way a 10 year old could understand.

What makes Cryptonary different from free crypto content on YouTube or Twitter?

Signal vs noise. We filter out 99.9% of garbage projects, provide data backed analysis, and have a proven track record of finding winners. Not to mention since Cryptonary's inception in 2017 we have never taken investment, sponsorship or partnership. Compare this to pretty much everyone else, no track record, and a long list of partnerships that cloud judgements.

Why is there no trial or refund policy?

We share highly sensitive, time-critical research. Once it's out, it can't be "returned." That's why membership is annual only. Crypto success takes time and commitment. If someone is not willing to invest 12 months into their future, there is no place for them at Cryptonary.

Do I get direct access to the Cryptonary team?

Yes. You will have 24/7 to the team that bought you BTC at $1,000, ETH at $70, and SOL at $10. Through our community chats, live Q&As, and member only channels, you can ask questions and interact directly with the team. Our team has over 50 years of combined experience which you can tap into every single day.

How often is content updated?

Daily. We provide real-time updates, weekly reports, emergency alerts, and live Q&As when the markets move fast. In crypto, the market moves fast, in Cryptonary, we move faster.

How does the 3X Value Guarantee work?

We stand behind the value of our research. If the documented upside from our published research during your 12-month membership does not exceed three times (3X) the annual subscription cost, you can request a full refund. Historical context: In every completed market cycle since 2017, cumulative documented upside has exceeded 10X this threshold.

TermsRecommended from Cryptonary