Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 43s

This Options Protocol is Silently Taking Off

Global options markets are massive, yet crypto options remain only a small fraction of that total. When Coinbase agreed to acquire Deribit for $2.9 billion, it showed what many investors were already starting to recognize: options could become one of crypto’s next major markets. Let’s dig deeper…

In this report:

- Why options still matter in crypto

- The evolution of on-chain options protocols

- How these platforms work

- Tokenomics, buybacks, and incentive alignment

- The competitive landscape and key risks

- A live options walkthrough

Disclaimer: This is not financial or investment advice. You are responsible for any capital-related decisions you make, and only you are accountable for the results.

A quick primer

We have covered options several times at Cryptonary over the years, and each time the category looked like it was on the verge of breaking out. It never did. That history is worth acknowledging, because it is part of why this time deserves a closer look rather than blind enthusiasm. The difference now is that the infrastructure actually exists, and the largest options venue in the world was recently acquired for $2.9 billion. But what if there is an equivalent of that venue, but with full benefits of onchain finance…Derive is the largest self-custodial options exchange in crypto. The protocol has been live for more than five years, processed over $22.97 billion in cumulative volume, and recorded no publicly reported security or insolvency incidents over that period. It currently accounts for an estimated 90% of onchain options volume. Built on its own OP Stack rollup that settles to Ethereum, Derive offers both options and perpetual futures through a central limit order book alongside an institutional RFQ (request for quote) system.

What makes the setup notable is how early the market still appears to be pricing the opportunity. Depending on the data source, Derive’s market cap sits between $88.3 million and $113.43 million, with a fully diluted valuation of roughly $170.16 million to $179.59 million. Against that, the protocol holds a $60.79 million treasury and has raised just $6.3 million in outside capital.

Over the last 30 days, options notional volume reached $1.253 billion, while annualized fees are running at $6.19 million and annualized revenue at roughly $4.1 million. A quarter of that revenue is directed into weekly DRV buybacks. Based on publicly available information, there does not appear to be a separate equity layer sitting ahead of tokenholders, which makes DRV look like the clearest instrument for capturing protocol upside.

For reference, Coinbase valued Deribit at $2.9 billion. Derive is obviously much smaller, but that comparison helps frame how wide the gap remains between current scale, market structure, and valuation.

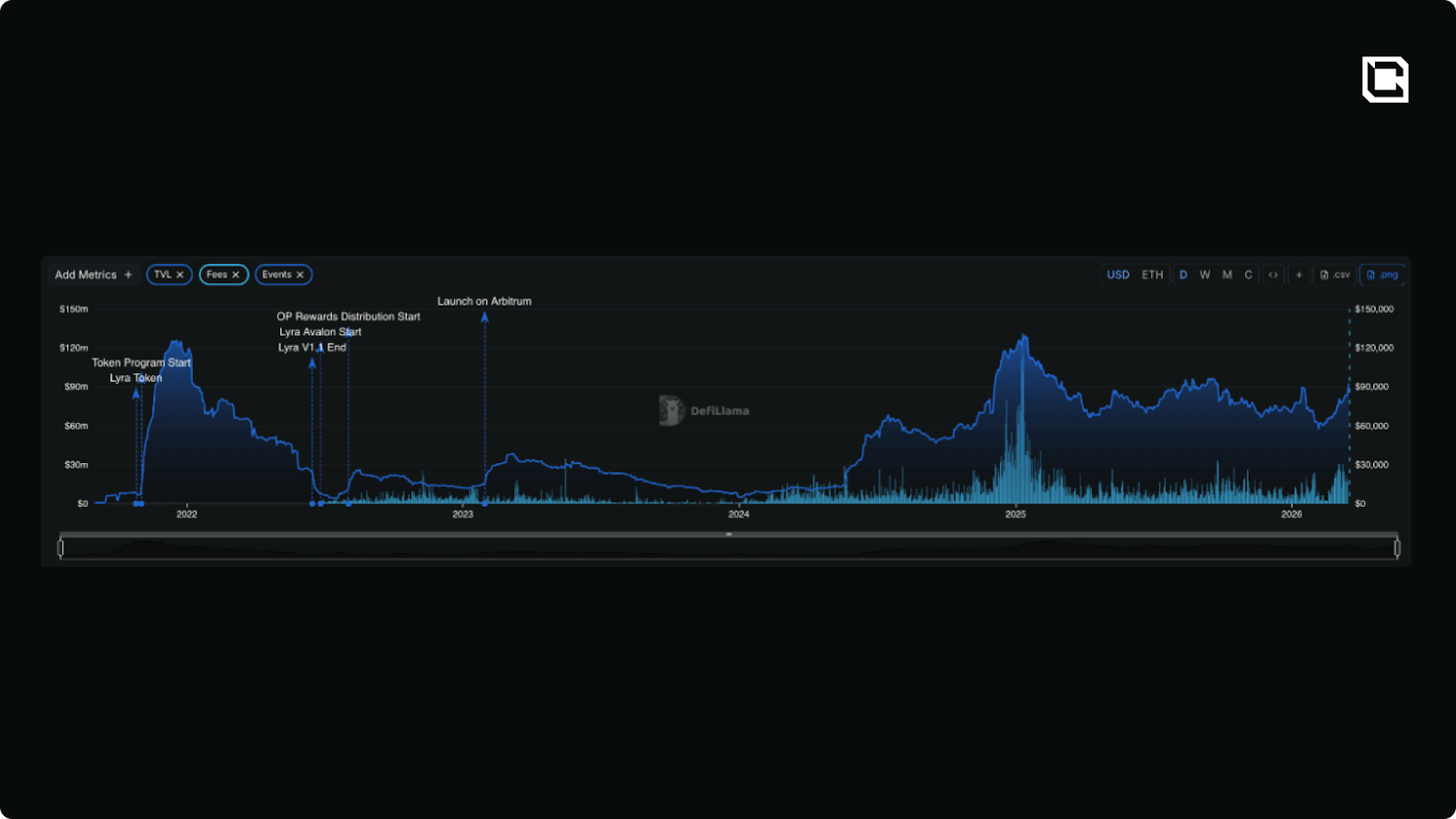

The protocol began in 2021 as Lyra Finance, founded by Nick Forster, a former Susquehanna options trader, alongside Michael Spain, Jake Fitzgerald, and Dom Romanowski. Lyra launched on Optimism as an AMM-based options protocol closely tied to the Synthetix ecosystem, using Black-Scholes pricing with market-driven implied volatility surfaces. The team raised a $3.3 million seed round led by Framework Ventures and ParaFi Capital, with participation from GSR.

By 2023, the limitations of the AMM model had become clear: capital inefficiency, impermanent loss, and difficulty delivering execution quality comparable to centralized venues. In response, the team migrated to its own OP Stack appchain and shifted to a central limit order book architecture. In September 2024, Lyra rebranded to Derive to reflect a broader ambition beyond options alone and toward a more complete onchain derivatives venue. The LYRA token migrated 1:1 into DRV in January 2025, with 56.38% of total supply coming from LYRA migration and 7.71% allocated through the airdrop.

Protocol pivots always carry execution risk, but Derive’s evolution also reflects something more valuable: a team that spent years operating in one of the hardest corners of DeFi, adapted when the original design hit its limits, and emerged with a functioning product, growing volume, and real category leadership.

Why Options Still Matter

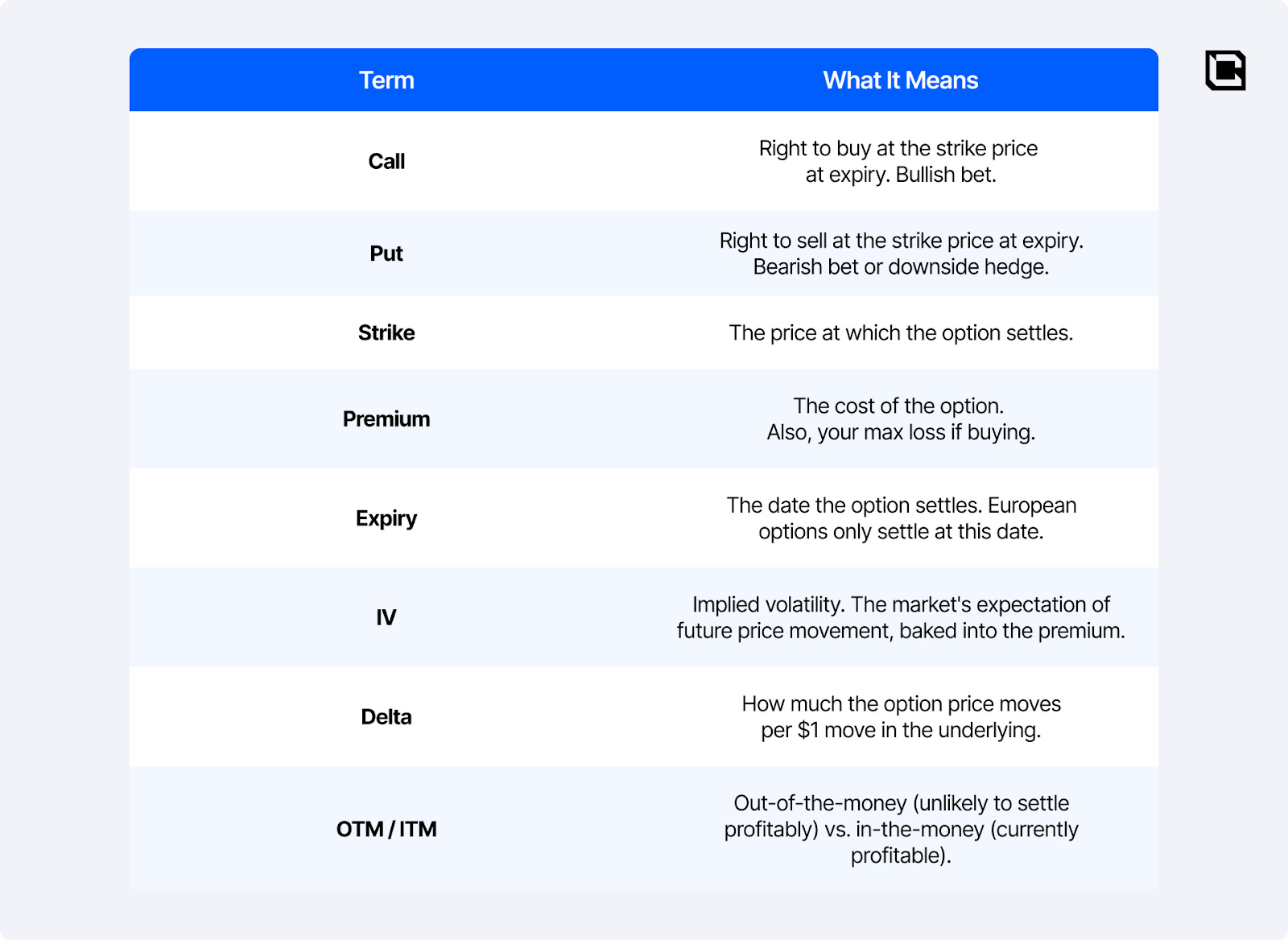

Options remain one of the last major areas of crypto market structure to fully mature. Spot markets came first, followed by the rapid rise of perpetuals. Options have lagged behind, partly because they are harder to explain, harder to market, and more demanding from both a liquidity and risk-management perspective. That does not make them irrelevant. It makes them early.An option is a contract that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a specific price, known as the strike, at expiry. The buyer pays a premium for that right. A call gives the right to buy at the strike and is typically used to express a bullish view.

A put gives the right to sell at the strike and is commonly used for bearish positioning or downside protection. For buyers of options, the maximum loss is the premium paid. In other words, the long option has defined downside from the outset. On Derive, options are European-style, meaning they settle only at expiry, with settlement based on a 30-minute TWAP of the underlying. That is broadly the same exercise standard used by Deribit.

Beyond simple directional bets, options unlock hedging, income generation, and non-linear payoff structures that let traders express views on volatility itself rather than just price direction. A fund holding large spot exposure can buy puts to define downside. A long-term holder can sell covered calls to monetize volatility. More advanced traders can build spreads, collars, and other structures that are simply not possible with spot alone, and only partially replicable with perps.

That is why options are treated in traditional markets as core infrastructure rather than a niche side product.

The total addressable market is what makes the category difficult to ignore. Crypto derivatives reached an estimated $8.94 trillion in monthly volume in 2025, yet options still represented only a small fraction of that activity. Crypto options remain small relative to both the broader derivatives complex and traditional options markets, and onchain options are smaller still. That is what makes the category so interesting: it remains underdeveloped, structurally harder to build, and far from saturated.

In more mature markets, options are not a side product. They are a core part of how traders hedge risk, express volatility views, and structure exposure with greater precision. Crypto has not reached that level of maturity yet, but the direction of travel is clear. Derive already commands a dominant share of the onchain segment, which means it operates in one of the few areas of crypto market structure that still looks genuinely early.

That is why the Coinbase-Deribit deal mattered so much. Coinbase announced its agreement to acquire Deribit in May 2025 for approximately $2.9 billion, consisting of $700 million in cash and 11 million Coinbase shares, and closed the transaction in August 2025. At the announcement, Coinbase described Deribit as the world’s leading crypto options venue, with roughly $30 billion of open interest and more than $1 trillion traded in 2024. By the time the deal closed, Coinbase said Deribit had roughly $60 billion of platform open interest and had just posted a record July with more than $185 billion in trading volume.

You do not pay $2.9 billion for a category you think is structurally unimportant.

The deal may also be shifting user behavior. Some desks will be perfectly comfortable staying with Deribit under Coinbase ownership. Others may prefer a venue that is self-custodial, onchain, and structurally separate from a large regulated U.S. exchange.

That does not guarantee a migration wave, but it does make the competitive landscape more interesting than it was a year ago. Derive’s architecture is explicitly built around that distinction: self-custodial trading, trustless settlement, an orderbook-based exchange layer, and protocol infrastructure deployed on its own OP Stack rollup.

How the Platform Works

At a high level, Derive is trying to offer the trading experience of a centralized exchange without requiring users to give up custody of their assets. Users place trades through an orderbook-style interface, while settlement and risk management happen onchain through Derive’s own rollup infrastructure. That gives users a mix of faster execution, transparent rules, and self-custody.The platform supports both options and perpetual futures, with portfolio margining across positions to improve capital efficiency. Rather than forcing traders to post separate collateral for every position, Derive evaluates the account as a whole, which can reduce capital requirements for hedged books and more complex strategies.

For bigger users, that matters because the pitch is not simply decentralization for its own sake. It is the ability to access a more capital-efficient, institution-friendly trading environment without sacrificing transparency or flexibility. The important point is that Derive is trying to bridge the gap between onchain infrastructure and the performance standards traders expect from centralized venues. That is the real point of the platform.

Now, let’s look at the tokenomics of DRV (Derive’s native token)

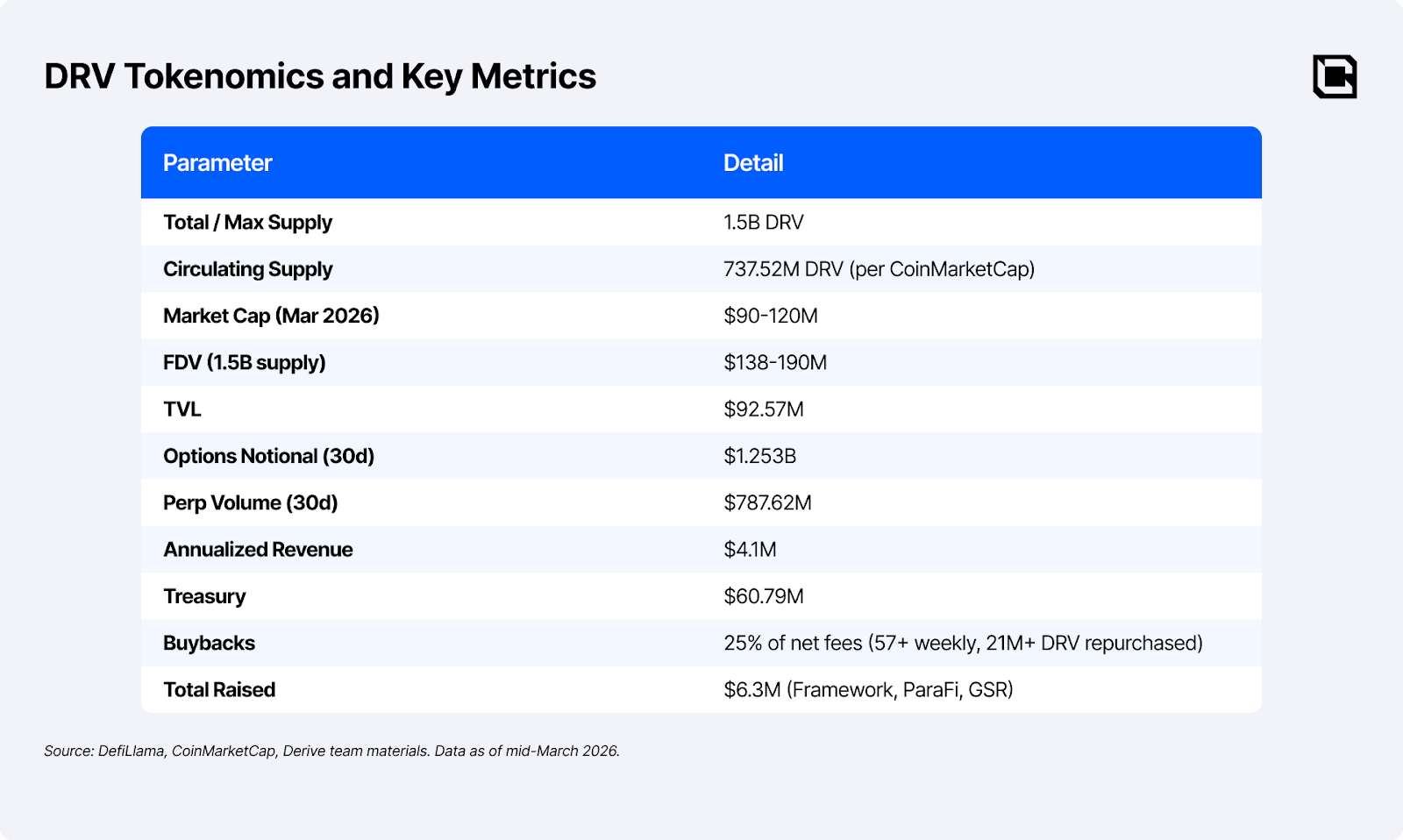

DRV Tokenomics and Key Metrics

The core tokenomic feature is the revenue link. Derive’s official DRV documentation says 25% of protocol revenue funds weekly DRV buybacks, while staking converts DRV into stDRV on Derive L2 with a 28-day unlock period or an instant unlock with a 20% penalty.

The same documentation says staking rewards were designed to begin at up to 1.15M DRV per week, step down to 600,000 after six months, and then transition toward buyback-funded rewards over time. Current market data shows 737.52M DRV circulating against 1.5B total supply and 1.5B max supply, which is the supply reality holders should use today.

The buyback mechanism is no longer theoretical. Recent buyback disclosures show weekly buyback #58 repurchased 203,528 DRV at an average price of $0.11, bringing cumulative repurchases to 21,514,713 DRV. Against the current 1.5B supply base, that amounts to a little over 1.4% of total supply bought back so far. More importantly, it shows that the mechanism is active, visible, and easy for tokenholders to monitor rather than existing only as a promise in the documentation.

The alignment structure is also worth highlighting. In the September 2025 strategic mint proposal, co-founder Nick Forster wrote that DRV is the sole alignment mechanism for contributors and partners and that there is no value-accruing equity associated with Derive-affiliated entities. If that framing is accurate, it makes DRV one of the cleaner tokenholder structures in DeFi. Governance, contributor incentives, and protocol economics all sit in the same instrument rather than being split between a token and a separate equity vehicle with competing claims on value accrual.

That said, dilution risk deserves to be stated directly. The original DRV help documentation described a 1.0B fixed supply and stated that no new tokens would be minted. But the September 2025 proposal explicitly sought authorization to mint an additional 500M DRV, a 50% increase that the proposal itself described as roughly 33% dilution to existing holders. Today, CoinMarketCap reflects 1.5B total supply and 1.5B max supply, which strongly suggests that the higher supply is now in effect in practice. That is the biggest tokenomic overhang in the story, and it should be treated as such.

Risks and Competition

We have been fans of Derive for quite some time, though we recognized that the options were ahead of their time. However, the competitive landscape seems to be changing now.The biggest competitive threat is Hyperliquid. On February 2, 2026, the network introduced HIP-4 on testnet, adding fully collateralized outcome contracts that settle within a fixed range. These products are closer to bounded, option-like outcome markets than to a full institutional options stack.

They do not yet replicate a traditional chain, richer Greeks-driven workflows, multi-leg tooling, or the kind of RFQ experience Derive is built around. But product completeness is only one part of the battle. Hyperliquid already has the attention, liquidity, user base, and ecosystem gravity that newer competitors struggle to match. Even if HIP-4 is narrower than a full options suite, it still pushes Hyperliquid further into the broader category of dated, non-linear derivatives.

If that happens, Derive could find itself competing not only against a strong product, but against the venue the market increasingly chooses first. That uncertainty remains the clearest reason we stay on monitor, not buy.

Deribit remains the undisputed benchmark. Official monthly statistics show $265.96 billion of turnover in October 2025, while Coinbase said Deribit had roughly $60 billion of platform open interest when the acquisition closed. Derive is not trying to replace Deribit head-to-head on raw scale or legacy market share. The more realistic path is to capture flow from traders and desks that want a neutral, self-custodial alternative with onchain settlement, not to displace the incumbent overnight.

Polymarket is worth mentioning here too, even though it is not an options protocol in name. Its monthly crypto markets, contracts like ‘Will BTC hit $80,000 in March?’, are structurally binary options. They have a strike (the price level), an expiry (end of month), a premium (the YES/NO price), and a defined max loss. The difference is that Polymarket strips away every piece of complexity that makes traditional options intimidating. There are no Greeks, no implied volatility columns, no chain to read. You just pick a price level, decide whether you think it gets hit, and buy. That simplicity is pulling real volume, with millions of dollars trading through the crypto monthly markets alone.

The reason this matters for Derive is not that Polymarket is a direct competitor for institutional options flow. It is that Polymarket is proving retail traders will engage with options-like payoff structures when the interface does not require a finance degree. The demand for this kind of product exists. The question is whether protocols like Derive can capture it with products that offer more flexibility without reintroducing all the complexity. Polymarket has shown what the addressable user base looks like when you remove the friction. That is both a validation of the broader thesis and a challenge for any protocol still presenting options in their raw form.

Live Trade Walkthrough

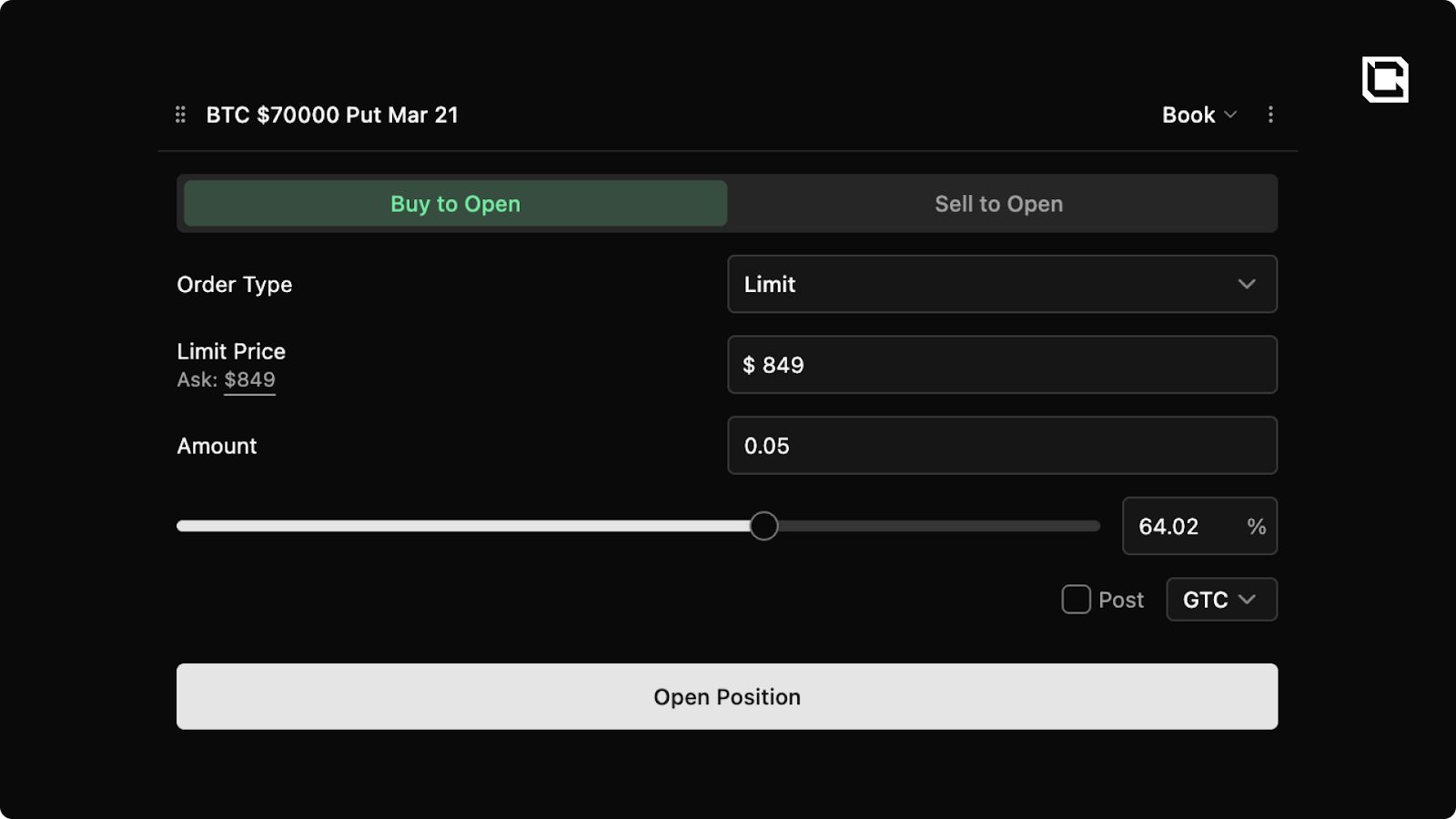

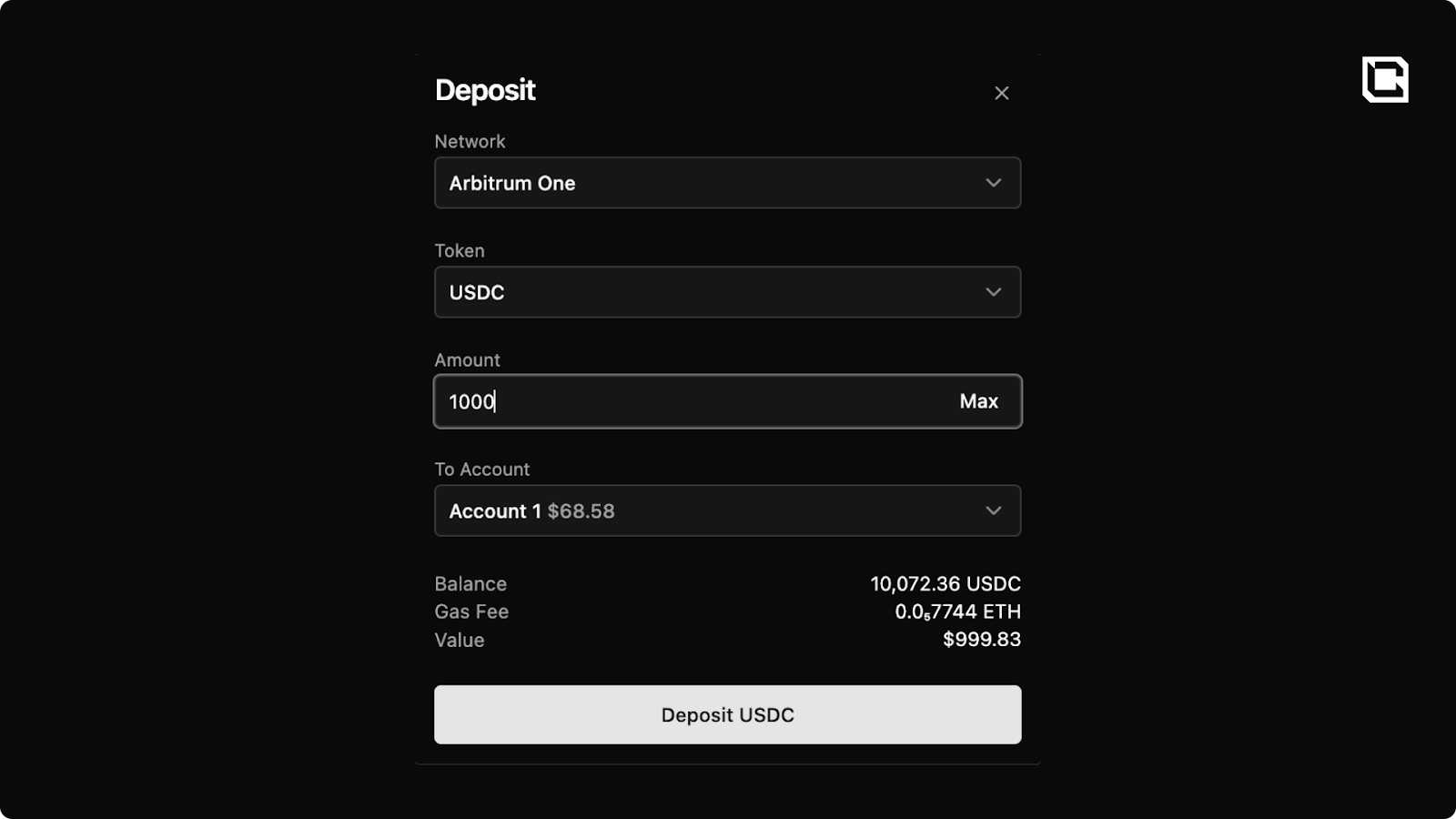

To show how Derive works in practice, it helps to start from the beginning at app.derive.xyz. After connecting a wallet, the first step is clicking the Deposit button in the top-right corner. In our example, collateral is deposited in USDC from Arbitrum One into the selected Derive account.

The process is straightforward: choose the network, token, amount, and destination account, then complete the approval and confirmation steps. Once the account is funded and trading is enabled, the balance becomes available for options and perps on the platform.

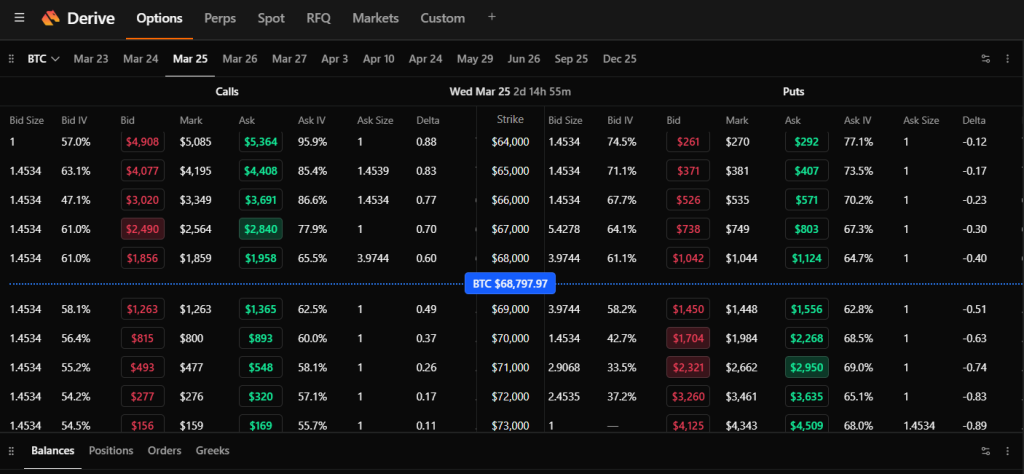

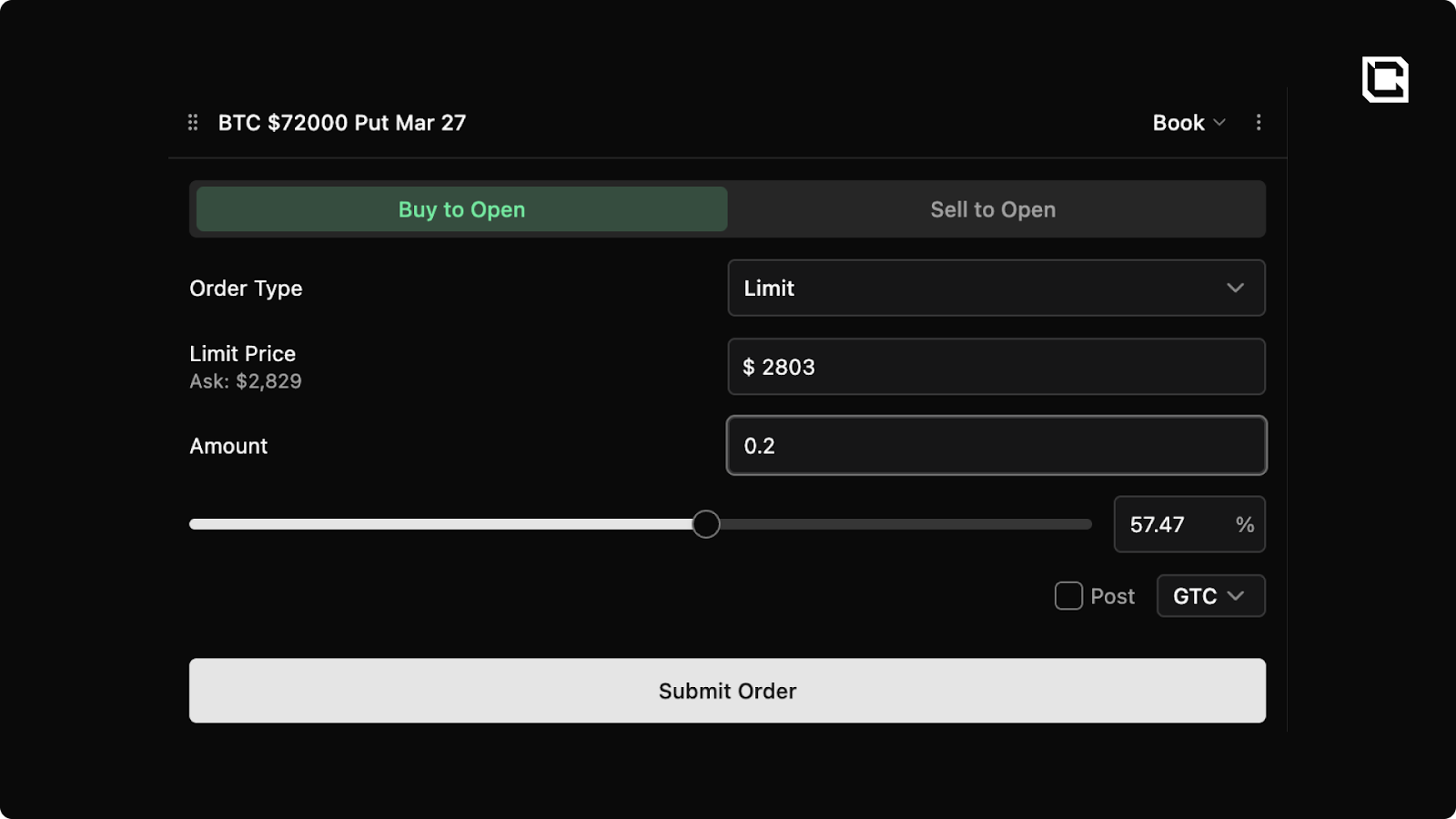

From there, the user moves to the Options page and selects the market and expiry. In this case, we use BTC options expiring on March 27. The option chain is organized with calls on the left, puts on the right, and strike prices in the middle.

The bid is the highest price a buyer is currently willing to pay, while the ask is the lowest price a seller is willing to accept. Bid size and ask size show how much liquidity is resting at those prices. In practice, clicking the ASK opens a LONG position, while clicking the BID opens a SHORT one.

For a simple single-leg example, we used a BTC March 27 $72,000 put, entered as Buy to Open. This is a straightforward bearish expression: if BTC falls, the put gains value, while the buyer’s maximum loss is limited to the premium paid. The order panel makes that easy to see before the trade is even placed. It shows the limit price, position size, maximum loss, breakeven, and the full payoff graph. That is one of the strongest parts of the interface: the risk-reward profile is visible immediately, rather than hidden behind the trade.

After selecting the trade, the payoff panel shows exactly where the position starts to make or lose money at expiry. In the case of the March 27 $72,000 put, the buyer begins to profit once BTC falls below the $69,317 breakeven shown on screen. One important detail is that the strike is not the same as the breakeven. The put starts to gain intrinsic value below the strike, but the trade only becomes profitable once that value exceeds the premium paid upfront. That is why the breakeven sits below the strike. If BTC finishes above the strike by expiry, the option expires worthless, and the buyer loses only the premium paid. That is the appeal of a long put: the downside is defined from the outset, while the position gains value as the market moves lower.

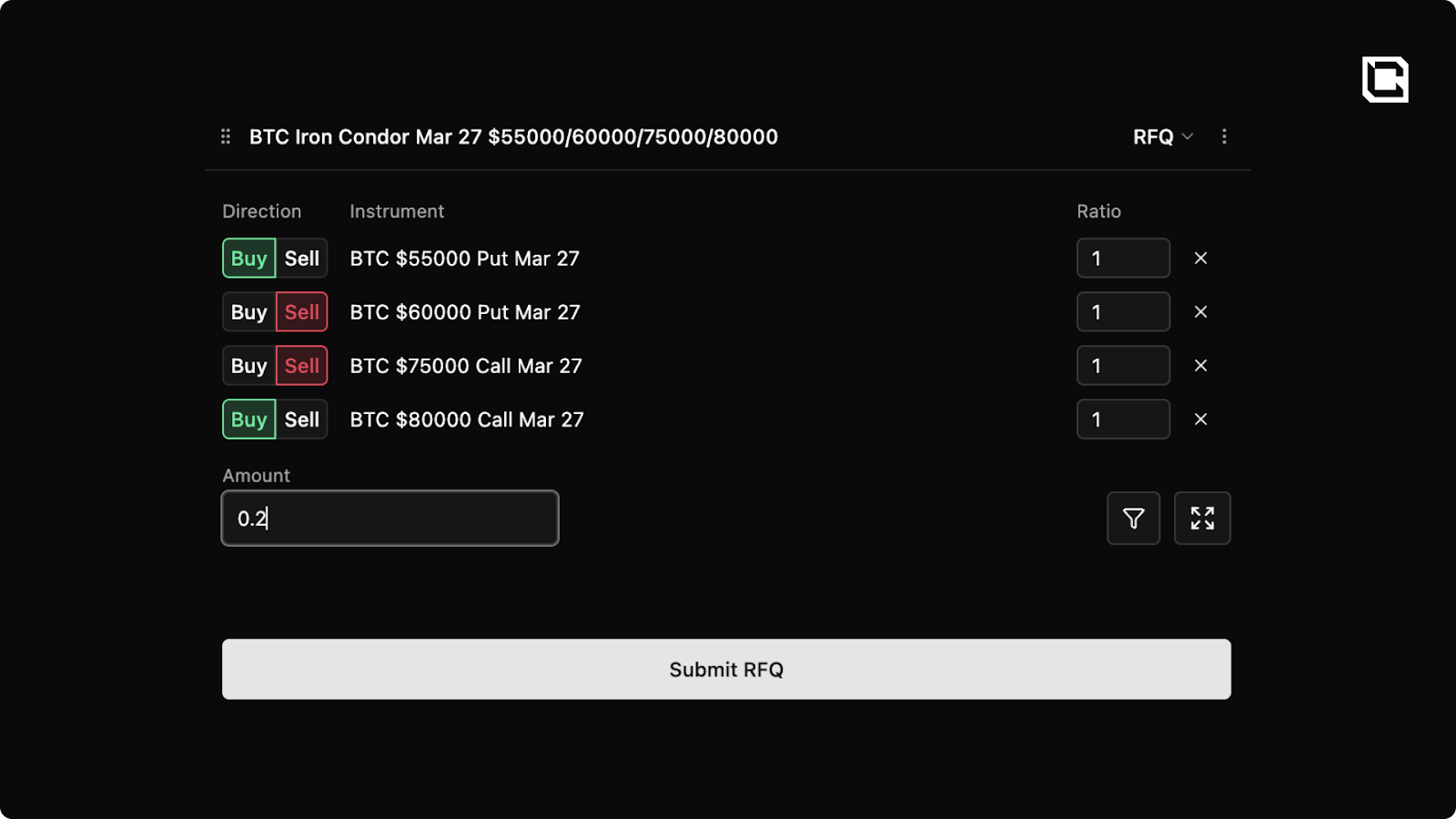

More advanced users can structure more nuanced views. To illustrate that flexibility, we also built a March 27 iron condor using a long $55,000 put, short $60,000 put, short $75,000 call, and long $80,000 call. The purpose here is not to suggest that this is the best trade, but to show what options can do beyond simple bullish or bearish bets. In this case, the position is designed to perform best if BTC remains roughly between $60,000 and $75,000 by expiry, while keeping downside defined on both sides. The payoff graph makes that clear at a glance.

The iron condor shows a different kind of flexibility. Based on the setup shown, the trade begins to lose money below about $59,388 on the downside and above about $75,612 on the upside, with losses capped beyond the long wings. In other words, the trader is not making a simple bullish or bearish bet, but expressing the view that BTC will stay within a range. That is where options become especially powerful: they allow traders to shape risk around a specific market view rather than forcing everything into a one-directional trade.

One of the most useful things about Derive’s interface is that these payoff shapes are visible before the trade is submitted. The graphs make it easier to understand where a position wins, where it loses, and how much is actually at risk. Just as importantly, the potential payoffs scale with position size. A trader can start small to learn the mechanics, then size up only when they are comfortable with how the structure behaves.

They are called options for a reason. They give traders more ways to express a market view than almost any other venue, whether that view is bullish, bearish, hedged, or range-bound. They can take a little time to get used to, but that flexibility is exactly what makes them so powerful. The best way to approach them is to start small, study the payoff, and experiment with different structures until the logic becomes intuitive.

Cryptonary’s Take

Derive is the clearest pure-play bet on the idea that crypto options eventually matter far more than they do today. It already leads the onchain category, has operated for years without any publicly reported security or insolvency incident, and sits in one of the few corners of DeFi where market structure still feels genuinely early. Most of crypto has already been priced, crowded, or commoditized. Onchain options have not.The fundamentals back that up. Derive has processed over $22.9 billion in cumulative volume, holds a $60.79 million treasury against a market cap in the $87 million to $120 million range, and runs a buyback mechanism that is not a whitepaper promise but a visible weekly reality. More than 21 million DRV have already been repurchased. Just as importantly, DRV appears to be the sole instrument through which holders capture protocol economics, with no obvious VC equity layer sitting ahead of them. When Coinbase paid $2.9 billion for Deribit, it validated the category. It also created a structural opening for a self-custodial alternative that Derive is better positioned to fill than anyone else in the space.

But being early is not the same as being de-risked. Hyperliquid is the clearest threat, not because HIP-4 is already a better options product, but because distribution often matters more than product purity. If Hyperliquid becomes the venue where liquidity, builders, and institutional attention consolidate, Derive could find itself competing against a stronger network rather than a weaker product. That is a very different challenge.

The second unresolved variable is dilution. Total supply has already expanded from 1 billion to 1.5 billion. The buyback mechanism is real, but it is now buying back tokens against a much larger supply base. Until the market fully digests that change and revenue scales meaningfully from here, the tokenomics story is less clean than it first appears.

What would move us off the sidelines? If Derive maintains or grows its share of onchain options volume through a potential HIP-4 mainnet launch, that would suggest the product moat is real and not just a first-mover advantage. If annualized revenue can scale materially from roughly $4.1 million as the category matures, the valuation starts to look genuinely cheap rather than merely optically interesting. And if the supply picture stabilizes with no further dilution, the alignment thesis becomes much stronger.

Until then, this remains a monitor, not a buy. But it is a serious one. Derive is not vaporware or a hollow narrative. It is a functioning protocol with real volume, real revenue, real buybacks, and exposure to one of the few market segments in crypto that still feels genuinely early. The question is not whether onchain options matter. It is whether Derive can hold its lead as the competition gets stronger.

Cryptonary, OUT!

Continue reading by joining Cryptonary Pro

$1,548 $1,197/year

Get everything you need to actively manage your portfolio and stay ahead. Ideal for investors seeking regular guidance and access to tools that help make informed decisions.

For your security, all orders are processed on a secured server.

As a Cryptonary Pro subscriber, you also get:

3X Value Guarantee - If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund. Terms

24/7 access to experts with 50+ years’ experience

All of our top token picks for 2025

On hand technical analysis on any token of your choice

Weekly livestreams & ask us anything with the team

Daily insights on Macro, Mechanics, and On-chain

Curated list of top upcoming airdrops (free money)

3X Value Guarantee

If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut through the noise and consistently find winning assets.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut

through the noise and consistently find winning assets.

Frequently Asked Questions

Can I trust Cryptonary's calls?

Yes. We've consistently identified winners across multiple cycles. Bitcoin under $1,000, Ethereum under $70, Solana under $10, WIF from $0.003 to $5, PopCat from $0.004 to $2, SPX blasting past $1.70, and our latest pick has already 200X'd since June 2025. Everything is timestamped and public record.

Do I need to be an experienced trader or investor to benefit?

No. When we founded Cryptonary in 2017 the market was new to everyone. We intentionally created content that was easy to understand and actionable. That foundational principle is the crux of Cryptonary. Taking complex ideas and opportunities and presenting them in a way a 10 year old could understand.

What makes Cryptonary different from free crypto content on YouTube or Twitter?

Signal vs noise. We filter out 99.9% of garbage projects, provide data backed analysis, and have a proven track record of finding winners. Not to mention since Cryptonary's inception in 2017 we have never taken investment, sponsorship or partnership. Compare this to pretty much everyone else, no track record, and a long list of partnerships that cloud judgements.

Why is there no trial or refund policy?

We share highly sensitive, time-critical research. Once it's out, it can't be "returned." That's why membership is annual only. Crypto success takes time and commitment. If someone is not willing to invest 12 months into their future, there is no place for them at Cryptonary.

Do I get direct access to the Cryptonary team?

Yes. You will have 24/7 to the team that bought you BTC at $1,000, ETH at $70, and SOL at $10. Through our community chats, live Q&As, and member only channels, you can ask questions and interact directly with the team. Our team has over 50 years of combined experience which you can tap into every single day.

How often is content updated?

Daily. We provide real-time updates, weekly reports, emergency alerts, and live Q&As when the markets move fast. In crypto, the market moves fast, in Cryptonary, we move faster.

How does the 3X Value Guarantee work?

We stand behind the value of our research. If the documented upside from our published research during your 12-month membership does not exceed three times (3X) the annual subscription cost, you can request a full refund. Historical context: In every completed market cycle since 2017, cumulative documented upside has exceeded 10X this threshold.

TermsRecommended from Cryptonary